Post-Double Selection

Last updated on Mar 9, 2022

# Remove warnings

import warnings

warnings.filterwarnings('ignore')

# Import everything

import pandas as pd

import numpy as np

import seaborn as sns

import statsmodels.api as sm

from numpy.linalg import inv

from statsmodels.iolib.summary2 import summary_col

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression, Lasso, Ridge

from sklearn.tree import DecisionTreeRegressor

from sklearn.ensemble import RandomForestRegressor, GradientBoostingRegressor

from sklearn.preprocessing import PolynomialFeatures, StandardScaler

# Import matplotlib for graphs

import matplotlib.pyplot as plt

from mpl_toolkits.mplot3d import axes3d

# Set global parameters

%matplotlib inline

plt.style.use('seaborn-white')

plt.rcParams['lines.linewidth'] = 3

plt.rcParams['figure.figsize'] = (10,6)

plt.rcParams['figure.titlesize'] = 20

plt.rcParams['axes.titlesize'] = 18

plt.rcParams['axes.labelsize'] = 14

plt.rcParams['legend.fontsize'] = 14

9.1 Frisch-Waugh theorem

Consider the data $D = { x_i, y_i, z_i }_{i=1}^n$ with DGP:

$$ y_i = x_i’ \alpha_0+ z_i’ \beta_0 + \varepsilon_i $$

. The following estimators of $\alpha$ are numerically equivalent (if $[x, z]$ has full rank):

- OLS: $\hat{\alpha}$ from regressing $y$ on $x, z$

- Partialling out: $\tilde{\alpha}$ from regressing $y$ on $\tilde{x}$

- “Double” partialling out: $\bar{\alpha}$ from regressing $\tilde{y}$ on $\tilde{x}$

where the operation of passing to $y, x$ to $\tilde{y}, \tilde{x}$ is called projection out $z$, e.g. $\tilde{x}$ are the residuals from regressing $x$ on $z$.

$$ \tilde{x} = x - \hat \gamma z = (I - z (z’ z)^{-1} z’ ) x = (I-P_z) x = M_z x $$

I.e we have done the following:

- regress $x$ on $z$

- compute $\hat x$

- compute the residuals $\tilde x = x - \hat x$

We now explore the theorem through simulation. In particular, we generate a sample from the following model:

$$ y_i = x_i - 0.3 z_i + \varepsilon_i $$

where $x_i,z_i,\varepsilon_i \sim N(0,1)$ and $n=1000$.

np.random.seed(1)

# Init

n = 1000

a = 1

b = -.3

# Generate data

x = np.random.uniform(0,1,n).reshape(-1,1)

z = np.random.uniform(0,1,n).reshape(-1,1)

e = np.random.normal(0,1,n).reshape(-1,1)

y = a*x + b*z + e

Let’s compute the value of the OLS estimator.

# Estimate alpha by OLS

xz = np.concatenate([x,z], axis=1)

ols_coeff = inv(xz.T @ xz) @ xz.T @ y

alpha_ols = ols_coeff[0][0]

print('alpha OLS: %.4f (true=%1.0f)' % (alpha_ols, a))

alpha OLS: 1.0928 (true=1)

The partialling out estimator.

# Partialling out

x_tilde = (np.eye(n) - z @ inv(z.T @ z) @ z.T ) @ x

alpha_po = inv(x_tilde.T @ x_tilde) @ x_tilde.T @ y

print('alpha partialling out: %.4f (true=%1.0f)' % (alpha_po, a))

alpha partialling out: 1.0928 (true=1)

And lastly, the double-partialling out estimator.

# "Double" partialling out

y_tilde = (np.eye(n) - z @ inv(z.T @ z) @ z.T ) @ y

alpha_po2 = inv(x_tilde.T @ x_tilde) @ x_tilde.T @ y_tilde

print('alpha double partialling out: %.4f (true=%1.0f)' % (alpha_po2, a))

alpha double partialling out: 1.0928 (true=1)

9.2 Omitted Variable Bias

Consider two separate statistical models. Assume the following long regression of interest:

$$ y_i = x_i’ \alpha_0+ z_i’ \beta_0 + \varepsilon_i $$

Define the corresponding short regression as

$$ y_i = x_i’ \alpha_0 + v_i \quad \text{ with } \quad x_i = z_i’ \gamma_0 + u_i $$

OVB Theorem

Suppose that the DGP for the long regression corresponds to $\alpha_0$, $\beta_0$. Suppose further that $\mathbb E[x_i] = 0$, $\mathbb E[z_i] = 0$, $\mathbb E[\varepsilon_i |x_i,z_i] = 0$. Then, unless $\beta_0 = 0$ or $z_i$ is orthogonal to $x_i$, the (sole) stochastic regressor $x_i$ is correlated with the error term in the short regression which implies that the OLS estimator of the short regression is inconsistent for $\alpha_0$ due to the omitted variable bias. In particular, one can show that the plim of the OLS estimator of $\hat{\alpha}_{SHORT}$ from the short regression is

$$ \hat{\alpha}_{SHORT} \overset{p}{\to} \frac{Cov(y_i, x_i)}{Var(x_i)} = \alpha_0 + \beta_0 \frac{Cov(z_i, x_i)}{Var(x_i)} $$

Consider data $D= (y_i, x_i, z_i)_{i=1}^n$, where the true model is:

$$ \begin{aligned} & y_i = x_i’ \alpha_0 + z_i’ \beta_0 + \varepsilon_i \ & x_i = z_i’ \gamma_0 + u_i \end{aligned} $$

Let’s investigate the Omitted Variable Bias by simulation. In particular, we generate a sample from the following model:

$$ \begin{aligned} & y_i = x_i - 0.3 z_i + \varepsilon_i \ & x_i = 3 z_i + u_i \ \end{aligned} $$

where $z_i,\varepsilon_i,u_i \sim N(0,1)$ and $n=1000$.

def generate_data(a, b, c, n):

# Generate data

z = np.random.normal(0,1,n).reshape(-1,1)

u = np.random.normal(0,1,n).reshape(-1,1)

x = c*z + u

e = np.random.normal(0,1,n).reshape(-1,1)

y = a*x + b*z + e

return x, y, z

First let’s compute the value of the OLS estimator.

# Init

n = 1000

a = 1

b = -.3

c = 3

x, y, z = generate_data(a, b, c, n)

# Estimate alpha by OLS

ols_coeff = inv(x.T @ x) @ x.T @ y

alpha_short = ols_coeff[0][0]

print('alpha OLS: %.4f (true=%1.0f)' % (alpha_short, a))

alpha OLS: 0.9115 (true=1)

In our case the expected bias is:

$$ \begin{aligned} Bias & = \beta_0 \frac{Cov(z_i, x_i)}{Var(x_i)} = \ & = \beta_0 \frac{Cov(z_i’ \gamma_0 + u_i, x_i)}{Var(z_i’ \gamma_0 + u_i)} = \ & = \beta_0 \frac{\gamma_0 Var(z_i)}{\gamma_0^2 Var(z_i) + Var(u_i)} \end{aligned} $$

which in our case is $b \frac{c}{c^2 + 1}$.

# Expected bias

bias = alpha_short - a

exp_bias = b * c / (c**2 + 1)

print('Empirical bias: %.4f \nExpected bias: %.4f' % (bias, exp_bias))

Empirical bias: -0.0885

Expected bias: -0.0900

9.3 Pre-Test Bias

Consider data $D= (y_i, x_i, z_i)_{i=1}^n$, where the true model is:

$$ \begin{aligned} & y_i = x_i’ \alpha_0 + z_i’ \beta_0 + \varepsilon_i \ & x_i = z_i’ \gamma_0 + u_i \end{aligned} $$

Where $x_i$ is the variable of interest (we want to make inference on $\alpha_0$) and $z_i$ is a high dimensional set of control variables.

From now on, we will work under the following assumptions:

- $\dim(x_i)=1$ for all $n$

- $\beta_0$ uniformely bounded in $n$

- Strict exogeneity: $\mathbb E[\varepsilon_i | x_i, z_i] = 0$ and $\mathbb E[u_i | z_i] = 0$

- $\beta_0$ and $\gamma_0$ have dimension (and hence value) that depend on $n$

Pre-Testing procedure:

- Regress $y_i$ on $x_i$ and $z_i$

- For each $j = 1, …, p = \dim(z_i)$ calculate a test statistic $t_j$

- Let $\hat{T} = { j: |t_j| > C > 0 }$ for some constant $C$ (set of statistically significant coefficients).

- Re-run the new “model” using $(x_i, z_{\hat{T},i})$ (i.e. using the selected covariates with statistically significant coefficients).

- Perform statistical inference (i.e. confidence intervals and hypothesis tests) as if no model selection had been done.

Pre-testing leads to incorrect inference. Why? Because of test errors in the first stage.

# T-test

def t_test(y, x, k):

beta_hat = inv(x.T @ x) @ x.T @ y

residuals = y - x @ beta_hat

sigma2_hat = np.var(residuals)

beta_std = np.sqrt(np.diag(inv(x.T @ x)) * sigma2_hat )

return beta_hat[k,0]/beta_std[k]

First of all the t-test for $H_0: \beta_0 = 0$:

$$ t = \frac{\hat \beta_k}{\hat \sigma_{\beta_k}} $$

where the standard deviation of the ols coefficient is given by

$$ \hat \sigma_{\beta_k} = \sqrt{ \hat \sigma^2 \cdot (X’X)^{-1}_{[k,k]} } $$

where we estimate the variance of the error term with the variance of the residuals

$$ \hat \sigma^2 = Var \big( y - \hat y \big) = Var \big( y - X (X’X)^{-1}X’y \big) $$

# Pre-testing

def pre_testing(a, b, c, n, simulations=1000):

np.random.seed(1)

# Init

alpha = {'Long': np.zeros((simulations,1)),

'Short': np.zeros((simulations,1)),

'Pre-test': np.zeros((simulations,1))}

# Loop over simulations

for i in range(simulations):

# Generate data

x, y, z = generate_data(a, b, c, n)

xz = np.concatenate([x,z], axis=1)

# Compute coefficients

alpha['Long'][i] = (inv(xz.T @ xz) @ xz.T @ y)[0][0]

alpha['Short'][i] = inv(x.T @ x) @ x.T @ y

# Compute significance of z on y

t = t_test(y, xz, 1)

# Select specification based on test

if np.abs(t)>1.96:

alpha['Pre-test'][i] = alpha['Long'][i]

else:

alpha['Pre-test'][i] = alpha['Short'][i]

return alpha

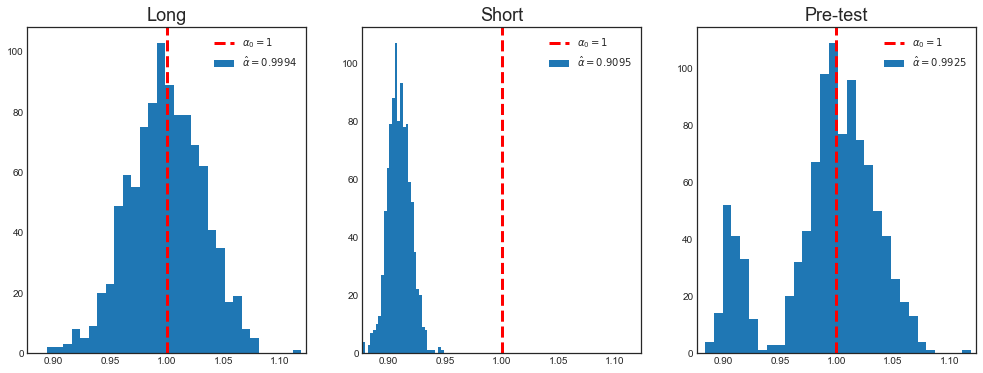

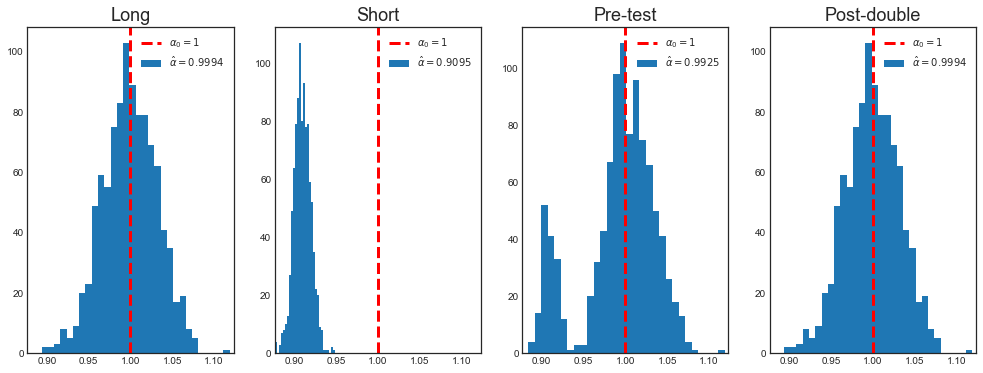

Let’s compare the different estimates.

# Get pre_test alpha

alpha = pre_testing(a, b, c, n)

for key, value in alpha.items():

print('Mean alpha %s = %.4f' % (key, np.mean(value)))

Mean alpha Long = 0.9994

Mean alpha Short = 0.9095

Mean alpha Pre-test = 0.9925

The pre-testing coefficient is very close to the true coefficient.

However, the main effect of pre-testing is on inference. With pre-testing, the distribution of the estimator is not gaussian anymore.

def plot_alpha(alpha, a):

fig = plt.figure(figsize=(17,6))

# Plot distributions

x_max = np.max([np.max(np.abs(x-a)) for x in alpha.values()])

# All axes

for i, key in enumerate(alpha.keys()):

# Reshape exisiting subplots

k = len(fig.axes)

for i in range(k):

fig.axes[i].change_geometry(1, k+1, i+1)

# Add new plot

ax = fig.add_subplot(1, k+1, k+1)

ax.hist(alpha[key], bins=30)

ax.set_title(key)

ax.set_xlim([a-x_max, a+x_max])

ax.axvline(a, c='r', ls='--')

legend_text = [r'$\alpha_0=%.0f$' % a, r'$\hat \alpha=%.4f$' % np.mean(alpha[key])]

ax.legend(legend_text, prop={'size': 10})

Let’s compare the long, short and pre-test estimators.

# Plot

plot_alpha(alpha, a)

As we can see, the main problem of pre-testing is inference.

Because of the testing procedure, the distribution of the estimator is a combination of tho different distributions: the one resulting from the long regression and the one resulting from the short regression. Pre-testing is not a problem in 3 cases:

-

when $\beta_0$ is very large: in this case the test always rejects the null hypothesis $H_0 : \beta_0=0$ and we always run the correct specification, i.e. the long regression

-

when $\beta_0$ is very small: in this case the test has very little power. However, as we saw from the Omitted Variable Bias formula, the bias is small.

-

when $\gamma_0$ is very small: also in this case the test has very little power. However, as we saw from the Omitted Variable Bias formula, the bias is small.

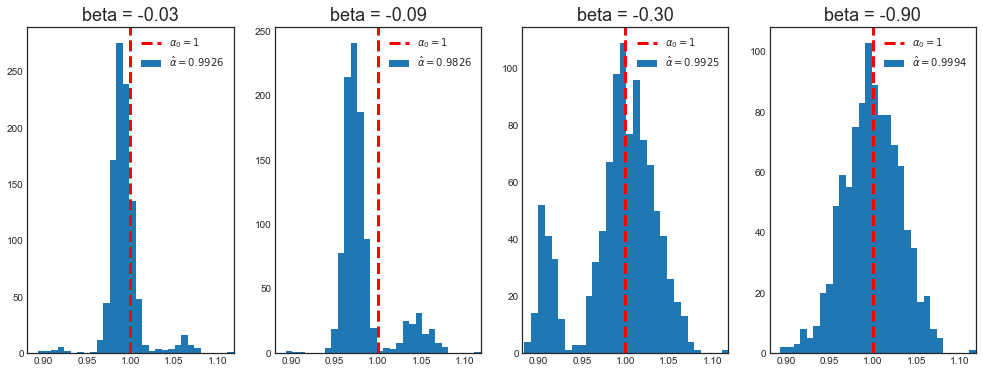

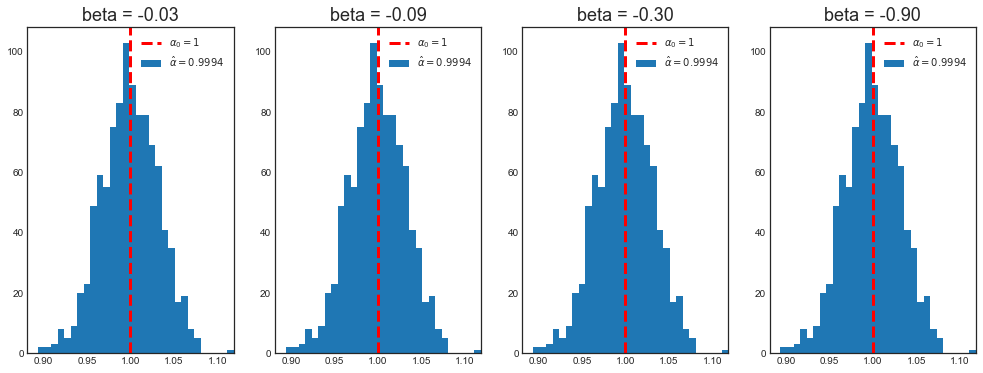

Let’s compare the pre-test estimates for different values of the true parameter $\beta$.

# Case 1: different betas and same sample size

b_sequence = b*np.array([0.1,0.3,1,3])

alpha = {}

# Get sequence

for k, b_ in enumerate(b_sequence):

label = 'beta = %.2f' % b_

alpha[label] = pre_testing(a, b_, c, n)['Pre-test']

print('Mean alpha with beta=%.2f: %.4f' % (b_, np.mean(alpha[label])))

Mean alpha with beta=-0.03: 0.9926

Mean alpha with beta=-0.09: 0.9826

Mean alpha with beta=-0.30: 0.9925

Mean alpha with beta=-0.90: 0.9994

The means are similar, but let’s look at the distributions.

# Plot

plot_alpha(alpha, a)

When $\beta_0$ is “small”, the distribution of the pre-testing estimator for $\alpha$ is not normal.

However, the magnitue of $\beta_0$ is a relative concept. For an infinite sample size, $\beta_0$ is always going to be “big enough”, in the sense that with an infinite sample size the probability fo false positives in testing $H_0: \beta_0 = 0$ is going to zero. I.e. we always select the correct model specification, the long regression.

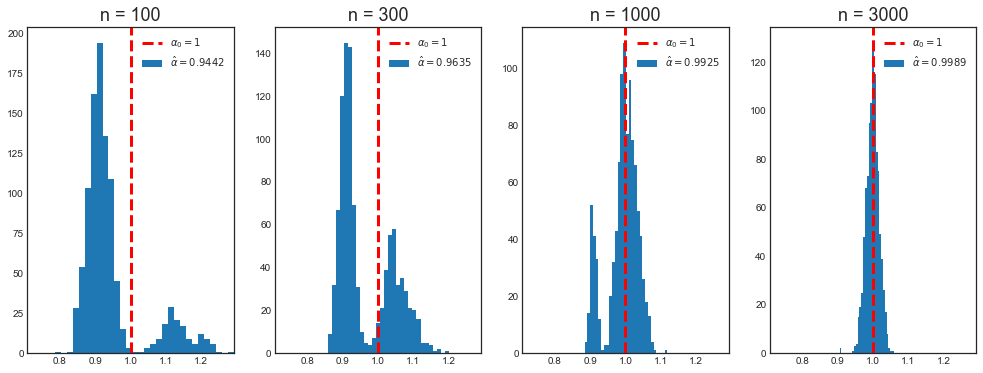

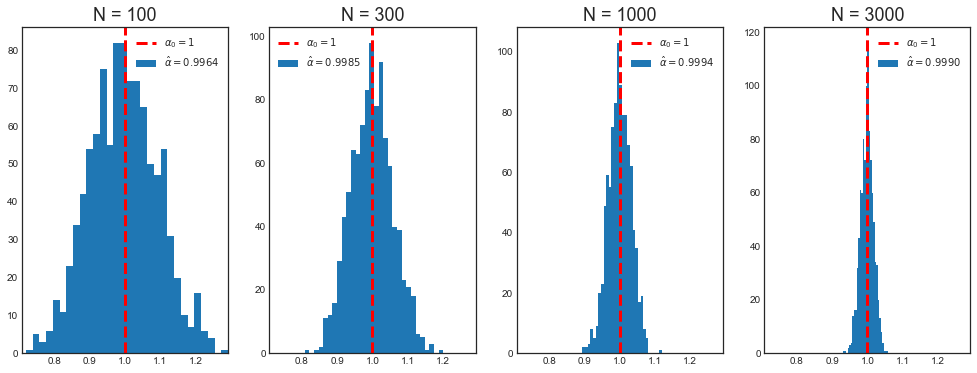

Let’s have a look at the distibution of $\hat \alpha_{\text{PRE-TEST}}$ when the sample size increaes.

# Case 2: same beta and different sample sizes

n_sequence = [100,300,1000,3000]

alpha = {}

# Get sequence

for k, n_ in enumerate(n_sequence):

label = 'n = %.0f' % n_

alpha[label] = pre_testing(a, b, c, n_)['Pre-test']

print('Mean alpha with n=%.0f: %.4f' % (n_, np.mean(alpha[label])))

Mean alpha with n=100: 0.9442

Mean alpha with n=300: 0.9635

Mean alpha with n=1000: 0.9925

Mean alpha with n=3000: 0.9989

# Plot

plot_alpha(alpha, a)

As we can see, for large samples, $\beta_0$ is never “small”. In the limit, when $n \to \infty$, the probability of false positives while testing $H_0: \beta_0 = 0$ goes to zero.

We face a dilemma:

- pre-testing is clearlly a problem in finite samples

- all our econometric results are based on the assumption that $n \to \infty$

The problem is solved by assuming that the value of $\beta_0$ depends on the sample size. This might seems like a weird assumption but is just to have an asymptotically meaningful concept of “big” and “small”.

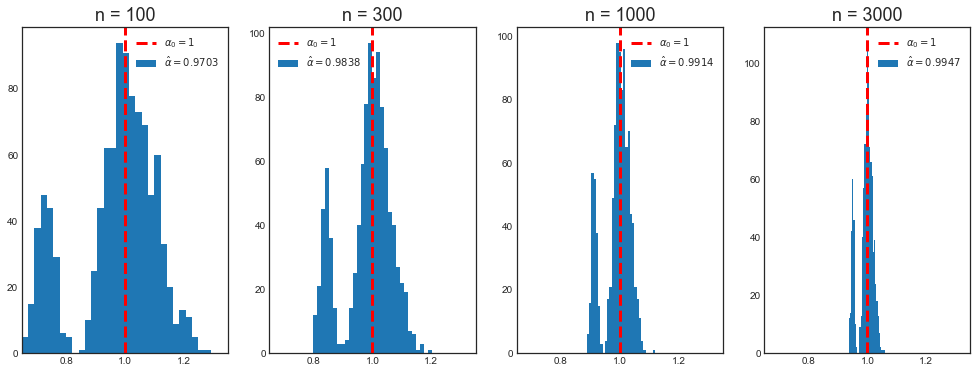

We now look at what happens in the simulations when $\beta_0$ is proportional to $\frac{1}{\sqrt{n}}$.

# Case 3: beta proportional to 1/sqrt(n) and different sample sizes

beta = b * 30 / np.sqrt(n_sequence)

# Get sequence

alpha = {}

for k, n_ in enumerate(n_sequence):

label = 'n = %.0f' % n_

alpha[label] = pre_testing(a, beta[k], c, n_)['Pre-test']

print('Mean alpha with n=%.0f: %.4f' % (n_, np.mean(alpha[label])))

Mean alpha with n=100: 0.9703

Mean alpha with n=300: 0.9838

Mean alpha with n=1000: 0.9914

Mean alpha with n=3000: 0.9947

# Plot

plot_alpha(alpha, a)

Now the distribution of $\hat \alpha$ does not converge to a normal when the sample size increases.

Pre-Testing and Machine Learning

How are machine learning and pre-testing related? The best example is Lasso. Suppose you have a dataset with many variables. This means that you have very few degrees of freedom and your OLS estimates are going to be very imprecise. At the extreme, you have more variables than observations so that your OLS coefficient is undefined since you cannot invert the design matrix $X’X$.

In this case, you might want to do variable selection. One way of doing variable selection is pre-testing. Another way is Lasso. A third alternative is to use machine learning methods that do not suffer this curse of dimensionality.

The purpose and outcome of pre-testing and Lasso are the same:

- you have too many variables

- you exclude some of them from the regression / set their coefficients to zero

As a consequence, also the problems are the same, i.e. pre-test bias.

9.4 Post-Double Selection

Consider again data $D= (y_i, x_i, z_i)_{i=1}^n$, where the true model is:

$$ \begin{aligned} & y_i = x_i’ \alpha_0 + z_i’ \beta_0 + \varepsilon_i \ & x_i = z_i’ \gamma_0 + u_i \end{aligned} $$

We would like to guard against pretest bias if possible, in order to handle high dimensional models. A good pathway towards motivating procedures which guard against pretest bias is a discussion of classical partitioned regression.

Consider a regression $y_i$ on $x_i$ and $z_i$. $x_i$ is the 1-dimensional variable of interest, $z_i$ is a high-dimensional set of control variables. We have the following procedure:

- First Stage selection: regress $x_i$ on $z_i$. Select the statistically significant variables in the set $S_{FS} \subseteq z_i$

- Reduced Form selection: lasso $y_i$ on $z_i$. Select the statistically significant variables in the set $S_{RF} \subseteq z_i$

- Regress $y_i$ on $x_i$ and $S_{FS} \cup S_{RF}$

Theorem: Let ${P^n}$ be a sequence of data-generating processes for $D_n = (y_i, x_i, z_i)^n_{i=1} \in (\mathbb R \times \mathbb R \times \mathbb R^p) ^n$ where $p$ depends on $n$. For each $n$, the data are iid with $yi = x_i’\alpha_0^{(n)} + z_i’ \beta_0^{(n)} + \varepsilon_i$ and $x_i = z_i’ \gamma_0^{(n)} + u_i$ where $\mathbb E[\varepsilon_i | x_i,z_i] = 0$ and $\mathbb E[u_i|z_i] = 0$. The sparsity of the vectors $\beta_0^{(n)}$, $\gamma_0^{(n)}$ is controlled by $|| \beta_0^{(n)} ||_0 \leq s$ with $s^2 (\log p)^2/n \to 0$. Suppose that additional regularity conditions on the model selection procedures and moments of the random variables $y_i$ , $x_i$ , $z_i$ as documented in Belloni et al. (2014). Then the confidence intervals, CI, from the post double selection procedure are uniformly valid. That is, for any confidence level $\xi \in (0, 1)$ $$ \Pr(\alpha_0 \in CI) \to 1- \xi $$

In order to have valid confidence intervals you want their bias to be negligibly. Since $$ CI = \left[ \hat{\alpha} \pm \frac{1.96 \cdot \hat{\sigma}}{\sqrt{n}} \right] $$

If the bias is $o \left( \frac{1}{\sqrt{n}} \right)$ then there is no problem since it is asymptotically negligible w.r.t. the magnitude of the confidence interval. If however the the bias is $O \left( \frac{1}{\sqrt{n}} \right)$ then it has the same magnitude of the confidence interval and it does not asymptotically vanish.

The idea of the proof is to use partitioned regression. An alternative way to think about the argument is: bound the omitted variables bias. Omitted variable bias comes from the product of 2 quantities related to the omitted variable:

- Its partial correlation with the outcome, and

- Its partial correlation with the variable of interest.

If both those partial correlations are $O( \sqrt{\log p/n})$, then the omitted variables bias is $(s \times O( \sqrt{\log p/n})^2 = o \left( \frac{1}{\sqrt{n}} \right)$, provided $s^2 (\log p)^2/n \to 0$. Relative to the $ \frac{1}{\sqrt{n}} $ convergence rate, the omitted variables bias is negligible.

In our omitted variable bias case, we want $| \beta_0 \gamma_0 | = o \left( \frac{1}{\sqrt{n}} \right)$. Post-double selection guarantees that

- Reduced form selection (pre-testing): any “missing” variable has $|\beta_{0j}| \leq \frac{c}{\sqrt{n}}$

- First stage selection (additional): any “missing” variable has $|\gamma_{0j}| \leq \frac{c}{\sqrt{n}}$

As a consequence, as long as the number of omitted variables is finite, the omitted variable bias is $$ OVB(\alpha) = |\beta_{0j}| \cdot|\gamma_{0j}| \leq \frac{c}{\sqrt{n}} \cdot \frac{c}{\sqrt{n}} = \frac{c^2}{n} = o \left(\frac{1}{\sqrt{n}}\right) $$

# Pre-testing code

def post_double_selection(a, b, c, n, simulations=1000):

np.random.seed(1)

# Init

alpha = {'Long': np.zeros((simulations,1)),

'Short': np.zeros((simulations,1)),

'Pre-test': np.zeros((simulations,1)),

'Post-double': np.zeros((simulations,1))}

# Loop over simulations

for i in range(simulations):

# Generate data

x, y, z = generate_data(a, b, c, n)

# Compute coefficients

xz = np.concatenate([x,z], axis=1)

alpha['Long'][i] = (inv(xz.T @ xz) @ xz.T @ y)[0][0]

alpha['Short'][i] = inv(x.T @ x) @ x.T @ y

# Compute significance of z on y (beta hat)

t1 = t_test(y, xz, 1)

# Compute significance of z on x (gamma hat)

t2 = t_test(x, z, 0)

# Select specification based on first test

if np.abs(t1)>1.96:

alpha['Pre-test'][i] = alpha['Long'][i]

else:

alpha['Pre-test'][i] = alpha['Short'][i]

# Select specification based on both tests

if np.abs(t1)>1.96 or np.abs(t2)>1.96:

alpha['Post-double'][i] = alpha['Long'][i]

else:

alpha['Post-double'][i] = alpha['Short'][i]

return alpha

Let’s now repeat the same exercise as above, but with also post-double selection

# Get pre_test alpha

alpha = post_double_selection(a, b, c, n)

for key, value in alpha.items():

print('Mean alpha %s = %.4f' % (key, np.mean(value)))

Mean alpha Long = 0.9994

Mean alpha Short = 0.9095

Mean alpha Pre-test = 0.9925

Mean alpha Post-double = 0.9994

# Plot

plot_alpha(alpha, a)

As we can see, post-double selection has solved the pre-testing problem. Does it work for any magnitude of $\beta$ (relative to the sample size)?

We first have a look at the case in which the sample size is fixed and $\beta_0$ changes.

# Case 1: different betas and same sample size

b_sequence = b*np.array([0.1,0.3,1,3])

alpha = {}

# Get sequence

for k, b_ in enumerate(b_sequence):

label = 'beta = %.2f' % b_

alpha[label] = post_double_selection(a, b_, c, n)['Post-double']

print('Mean alpha with beta=%.2f: %.4f' % (b_, np.mean(alpha[label])))

Mean alpha with beta=-0.03: 0.9994

Mean alpha with beta=-0.09: 0.9994

Mean alpha with beta=-0.30: 0.9994

Mean alpha with beta=-0.90: 0.9994

# Plot

plot_alpha(alpha, a)

Post-double selection always selects the correct specification, the long regression, even when $\beta$ is very small.

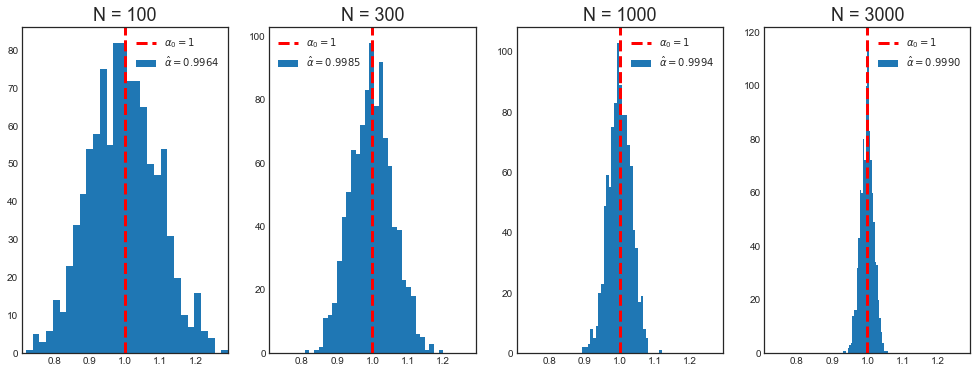

Now we check the same but for fixed $\beta_0$ and different sample sizes.

# Case 2: same beta and different sample sizes

n_sequence = [100,300,1000,3000]

alpha = {}

# Get sequence

for k, n_ in enumerate(n_sequence):

label = 'N = %.0f' % n_

alpha[label] = post_double_selection(a, b, c, n_)['Post-double']

print('Mean alpha with n=%.0f: %.4f' % (n_, np.mean(alpha[label])))

Mean alpha with n=100: 0.9964

Mean alpha with n=300: 0.9985

Mean alpha with n=1000: 0.9994

Mean alpha with n=3000: 0.9990

# Plot

plot_alpha(alpha, a)

Post-double selection always selects the correct specification, the long regression, even when the sample size is very small.

Last, we check the case of $\beta_0$ proportional to $\frac{1}{\sqrt{n}}$.

# Case 3: beta proportional to 1/sqrt(n) and different sample sizes

beta = b * 30 / np.sqrt(n_sequence)

# Get sequence

alpha = {}

for k, n_ in enumerate(n_sequence):

label = 'N = %.0f' % n_

alpha[label] = post_double_selection(a, beta[k], c, n_)['Post-double']

print('Mean alpha with n=%.0f: %.4f' % (n_, np.mean(alpha[label])))

Mean alpha with n=100: 0.9964

Mean alpha with n=300: 0.9985

Mean alpha with n=1000: 0.9994

Mean alpha with n=3000: 0.9990

# Plot

plot_alpha(alpha, a)

Once again post-double selection always selects the correct specification, the long regression.

Post-double Selection and Machine Learning

As we have seen at the end of the previous section, Lasso can be used to perform variable selection in high dimensional settings. Therefore, post-double selection solves the pre-test bias problem in those settings. The post-double selection procedure with Lasso is:

- First Stage selection: lasso $x_i$ on $z_i$. Let the selected variables be collected in the set $S_{FS} \subseteq z_i$

- Reduced Form selection: lasso $y_i$ on $z_i$. Let the selected variables be collected in the set $S_{RF} \subseteq z_i$

- Regress $y_i$ on $x_i$ and $S_{FS} \cup S_{RF}$

9.5 Double/debiased Machine Learning

This section is taken from Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., & Robins, J. (2018). “Double/debiased machine learning for treatment and structural parameters”.

Consider the following partially linear model

$$ y = \beta_0 D + g_0(X) + u \ D = m_0(X) + v $$

where $y$ is the outcome variable, $D$ is the treatment to interest and $X$ is a potentially high-dimensional set of controls.

Naive approach

A naive approach to estimation of $\beta_0$ using ML methods would be, for example, to construct a sophisticated ML estimator $\beta_0 D + g_0(X)$ for learning the regression function $\beta_0 D$ + $g_0(X)$.

- Split the sample in two: main sample and auxiliary sample

- Use the auxiliary sample to estimate $\hat g_0(X)$

- Use the main sample to compute the orthogonalized component of $Y$ on $X$: $\hat u = \left(Y_{i}-\hat{g}{0}\left(X{i}\right)\right)$

- Use the main sample to estimate the residualized OLS estimator

$$ \hat{\beta}{0}=\left(\frac{1}{n} \sum{i \in I} D_{i}^{2}\right)^{-1} \frac{1}{n} \sum_{i \in I} D_{i} \hat u_i $$

This estimator is going to have two problems:

- Slow rate of convergence, i.e. slower than $\sqrt(n)$

- It will be biased because we are employing highdimensional regularized estimators (e.g. we are doing variable selection)

Orthogonalization

Now consider a second construction that employs an orthogonalized formulation obtained by directly partialling out the effect of $X$ from $D$ to obtain the orthogonalized regressor $v = D − m_0(X)$.

-

Split the sample in two: main sample and auxiliary sample

-

Use the auxiliary sample to estimate $\hat g_0(X)$ from

$$ y = \beta_0 D + g_0(X) + u \ $$

-

Use the auxiliary sample to estimate $\hat m_0(X)$ from

$$ D = m_0(X) + v $$

-

Use the main sample to compute the orthogonalized component of $D$ on $X$ as

$$ \hat v = D - \hat m_0(X) $$

-

Use the main sample to estimate the double-residualized OLS estimator as

$$ \hat{\beta}{0}=\left(\frac{1}{n} \sum{i \in I} \hat v_i D_{i} \right)^{-1} \frac{1}{n} \sum_{i \in I} \hat v_i \left( Y - \hat g_0(X) \right) $$

The estimator is unbiased but still has a lower rate of convergence because of sample splitting. The problem is solved by inverting the split sample, re-estimating the coefficient and averaging the two estimates. Note that this procedure is valid since the two estimates are independent by the sample splitting procedure.

Application to AJR02

In this section we are going to replicate 6.3 of the “Double/debiased machine learning” paper based on Acemoglu, Johnson, Robinson (2002), “The Colonial Origins of Comparative Development”.

We first load the dataset

# Load Acemoglu Johnson Robinson Dataset

df = pd.read_csv('data/AJR02.csv',index_col=0)

df.head()

| GDP | Exprop | Mort | Latitude | Neo | Africa | Asia | Namer | Samer | logMort | Latitude2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 8.39 | 6.50 | 78.20 | 0.3111 | 0 | 1 | 0 | 0 | 0 | 4.359270 | 0.096783 |

| 2 | 7.77 | 5.36 | 280.00 | 0.1367 | 0 | 1 | 0 | 0 | 0 | 5.634790 | 0.018687 |

| 3 | 9.13 | 6.39 | 68.90 | 0.3778 | 0 | 0 | 0 | 0 | 1 | 4.232656 | 0.142733 |

| 4 | 9.90 | 9.32 | 8.55 | 0.3000 | 1 | 0 | 0 | 0 | 0 | 2.145931 | 0.090000 |

| 5 | 9.29 | 7.50 | 85.00 | 0.2683 | 0 | 0 | 0 | 1 | 0 | 4.442651 | 0.071985 |

df.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 64 entries, 1 to 64

Data columns (total 11 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 GDP 64 non-null float64

1 Exprop 64 non-null float64

2 Mort 64 non-null float64

3 Latitude 64 non-null float64

4 Neo 64 non-null int64

5 Africa 64 non-null int64

6 Asia 64 non-null int64

7 Namer 64 non-null int64

8 Samer 64 non-null int64

9 logMort 64 non-null float64

10 Latitude2 64 non-null float64

dtypes: float64(6), int64(5)

memory usage: 6.0 KB

In their paper, AJR note that their IV strategy will be invalidated if other factors are also highly persistent and related to the development of institutions within a country and to the country’s GDP. A leading candidate for such a factor, as they discuss, is geography. AJR address this by assuming that the confounding effect of geography is adequately captured by a linear term in distance from the equator and a set of continent dummy variables.

They inclue their results in table 2.

# Add constant term to dataset

df['const'] = 1

# Create lists of variables to be used in each regression

X1 = df[['const', 'Exprop']]

X2 = df[['const', 'Exprop', 'Latitude', 'Latitude2']]

X3 = df[['const', 'Exprop', 'Latitude', 'Latitude2', 'Asia', 'Africa', 'Namer', 'Samer']]

y = df['GDP']

# Estimate an OLS regression for each set of variables

reg1 = sm.OLS(y, X1, missing='drop').fit()

reg2 = sm.OLS(y, X2, missing='drop').fit()

reg3 = sm.OLS(y, X3, missing='drop').fit()

Let’s replicate Table 2 in AJR.

# Make table 2

def make_table_2():

info_dict={'No. observations' : lambda x: f"{int(x.nobs):d}"}

results_table = summary_col(results=[reg1,reg2,reg3],

float_format='%0.2f',

stars = True,

model_names=['Model 1','Model 2','Model 3'],

info_dict=info_dict,

regressor_order=['const','Exprop','Latitude','Latitude2'])

return results_table

table_2 = make_table_2()

table_2

| Model 1 | Model 2 | Model 3 | |

|---|---|---|---|

| const | 4.66*** | 4.55*** | 5.95*** |

| (0.41) | (0.45) | (0.68) | |

| Exprop | 0.52*** | 0.49*** | 0.40*** |

| (0.06) | (0.07) | (0.06) | |

| Latitude | 2.16 | 0.42 | |

| (1.68) | (1.47) | ||

| Latitude2 | -2.12 | 0.44 | |

| (2.86) | (2.48) | ||

| Africa | -1.06** | ||

| (0.41) | |||

| Asia | -0.74* | ||

| (0.42) | |||

| Namer | -0.17 | ||

| (0.40) | |||

| Samer | -0.12 | ||

| (0.42) | |||

| No. observations | 64 | 64 | 64 |

Using DML allows us to relax this assumption and to replace it by a weaker assumption that geography can be sufficiently controlled by an unknown function of distance from the equator and continent dummies, which can be learned by ML methods.

In particular, our framework is

$$ {GDP} = \beta_0 \times {Exprop} + g_0({geography}) + u \ {Exprop} = m_0({geography}) + u $$

So that the double/debiased machine learning procedure is

-

Split the sample in two: main sample and auxiliary sample

-

Use the auxiliary sample to estimate $\hat g_0({geography})$ from

$$ {GDP} = \beta_0 \times {Exprop} + g_0({geography}) + u $$

-

Use the auxiliary sample to estimate $\hat m_0({geography})$ from

$$ {Exprop} = m_0({geography}) + v $$

-

Use the main sample to compute the orthogonalized component of ${Exprop}$ on ${geography}$ as

$$ \hat v = {Exprop} - \hat m_0({geography}) $$

-

Use the main sample to estimate the double-residualized OLS estimator as

$$ \hat{\beta}{0}=\left(\frac{1}{n} \sum{i \in I} \hat v_i \times {Exprop}{i} \right)^{-1} \frac{1}{n} \sum{i \in I} \hat v_i \times \left( {GDP} - \hat g_0({geography}) \right) $$

Since we employ an intrumental variable strategy, we replace $m_0({geography})$ with $m_0({geography},{logMort})$ in the first stage.

# Generate variables

D = df['Exprop'].values.reshape(-1,1)

X = df[['const', 'Latitude', 'Latitude2', 'Asia', 'Africa', 'Namer', 'Samer']].values

y = df['GDP'].values.reshape(-1,1)

Z = df[['const', 'Latitude', 'Latitude2', 'Asia', 'Africa', 'Namer', 'Samer','logMort']].values

def estimate_beta(algorithm, alg_name, D, X, y, Z, sample):

# Split sample

D_main, D_aux = (D[sample==1], D[sample==0])

X_main, X_aux = (X[sample==1], X[sample==0])

y_main, y_aux = (y[sample==1], y[sample==0])

Z_main, Z_aux = (Z[sample==1], Z[sample==0])

# Residualize y on D

b_hat = inv(D_aux.T @ D_aux) @ D_aux.T @ y_aux

y_resid_aux = y_aux - D_aux @ b_hat

# Estimate g0

alg_fitted = algorithm.fit(X=X_aux, y=y_resid_aux.ravel())

g0 = alg_fitted.predict(X_main).reshape(-1,1)

# Compute v_hat

u_hat = y_main - g0

# Estimate m0

alg_fitted = algorithm.fit(X=Z_aux, y=D_aux.ravel())

m0 = algorithm.predict(Z_main).reshape(-1,1)

# Compute u_hat

v_hat = D_main - m0

# Estimate beta

beta = inv(v_hat.T @ D_main) @ v_hat.T @ u_hat

return beta

def ddml(algorithm, alg_name, D, X, y, Z, p=0.5, verbose=False):

# Expand X if Lasso or Ridge

if alg_name in ['Lasso ','Ridge ']:

X = PolynomialFeatures(degree=2).fit_transform(X)

# Generate split (fixed proportions)

split = np.array([i in train_test_split(range(len(D)), test_size=p)[0] for i in range(len(D))])

# Compute beta

beta = [estimate_beta(algorithm, alg_name, D, X, y, Z, split==k) for k in range(2)]

beta = np.mean(beta)

# Print and return

if verbose:

print('%s : %.4f' % (alg_name, beta))

return beta

# Generate sample split

p = 0.5

split = np.random.binomial(1, p, len(D))

We inspect different algorithms. In particular, we consider:

- Lasso Regression

- Ridge Regression

- Regression Trees

- Random Forest

- Boosted Forests

# List all algorithms

algorithms = {'Ridge ': Ridge(alpha=.1),

'Lasso ': Lasso(alpha=.01),

'Tree ': DecisionTreeRegressor(),

'Forest ': RandomForestRegressor(n_estimators=30),

'Boosting': GradientBoostingRegressor(n_estimators=30)}

Let’s compare the results.

# Loop over algorithms

for alg_name, algorithm in algorithms.items():

ddml(algorithm, alg_name, D, X, y, Z, verbose=True)

Ridge : 0.1289

Lasso : -8.7963

Tree : 1.2879

Forest : 2.4938

Boosting : 0.5977

The results are extremely volatile.

# Repeat K times

def estimate_beta_median(algorithms, D, X, y, Z, K):

# Loop over algorithms

for alg_name, algorithm in algorithms.items():

betas = []

# Iterate n times

for k in range(K):

beta = ddml(algorithm, alg_name, D, X, y, Z)

betas = np.append(betas, beta)

print('%s : %.4f' % (alg_name, np.median(betas)))

Let’s try using the median to have a more stable estimator.

np.random.seed(123)

# Repeat 100 times and take median

estimate_beta_median(algorithms, D, X, y, Z, 100)

Ridge : 0.6670

Lasso : 1.2511

Tree : 0.9605

Forest : 0.5327

Boosting : 1.0327

The results differ slightly from the ones in the paper, but they are at least closer.