Model Selection and Regularization

Last updated on Mar 9, 2022

# Remove warnings

import warnings

warnings.filterwarnings('ignore')

# Import

import pandas as pd

import numpy as np

import time

import itertools

import statsmodels.api as sm

import seaborn as sns

from numpy.random import normal, uniform

from itertools import combinations

from statsmodels.api import add_constant

from statsmodels.regression.linear_model import OLS

from sklearn.linear_model import LinearRegression, Ridge, Lasso, RidgeCV, LassoCV

from sklearn.cross_decomposition import PLSRegression, PLSSVD

from sklearn.model_selection import KFold, cross_val_score, train_test_split, LeaveOneOut, ShuffleSplit

from sklearn.preprocessing import scale

from sklearn.decomposition import PCA

from sklearn.metrics import mean_squared_error

# Import matplotlib for graphs

import matplotlib.pyplot as plt

from mpl_toolkits.mplot3d import axes3d

# Set global parameters

%matplotlib inline

plt.style.use('seaborn-white')

plt.rcParams['lines.linewidth'] = 3

plt.rcParams['figure.figsize'] = (12,5)

plt.rcParams['figure.titlesize'] = 20

plt.rcParams['axes.titlesize'] = 18

plt.rcParams['axes.labelsize'] = 14

plt.rcParams['legend.fontsize'] = 14

When we talk about big data, we do not only talk about bigger sample size, $n$, but also about a larger number of explanatory variables, $p$. However, with ordinary least squares, we are limited by the identification constraint that $p < n$. Moreover, for inference and prediction accuracy, we would actually like to have $k « n$.

This session adresses methods to use a least squares fit in a setting in which the number of regressors, $p$, is large with respect to the sample size, $n$

5.1 Subset Selection

The Subset Selection approach involves identifying a subset of the $p$ predictors that we believe to be related to the response. We then fit a model using least squares on the reduced set of variables.

Let’s load the credit rating dataset.

# Credit ratings dataset

credit = pd.read_csv('data/Credit.csv', usecols=list(range(1,12)))

credit.head()

| Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 14.891 | 3606 | 283 | 2 | 34 | 11 | Male | No | Yes | Caucasian | 333 |

| 1 | 106.025 | 6645 | 483 | 3 | 82 | 15 | Female | Yes | Yes | Asian | 903 |

| 2 | 104.593 | 7075 | 514 | 4 | 71 | 11 | Male | No | No | Asian | 580 |

| 3 | 148.924 | 9504 | 681 | 3 | 36 | 11 | Female | No | No | Asian | 964 |

| 4 | 55.882 | 4897 | 357 | 2 | 68 | 16 | Male | No | Yes | Caucasian | 331 |

We are going to look at the relationship between individual characteristics and account Balance in the Credit dataset.

# X and y

X = credit.loc[:, credit.columns != 'Balance']

y = credit.loc[:,'Balance']

Best Subset Selection

To perform best subset selection, we fit a separate least squares regression for each possible combination of the $p$ predictors. That is, we fit all $p$ models that contain exactly one predictor, all $p = p(p−1)/2$ models that contain 2 exactly two predictors, and so forth. We then look at all of the resulting models, with the goal of identifying the one that is best.

Clearly the main disadvantage of best subset selection is computational power.

def model_selection(X, y, *args):

# Init

scores = list(itertools.repeat(np.zeros((0,2)), len(args)))

# Categorical variables

categ_cols = {"Gender", "Student", "Married", "Ethnicity"}

# Loop over all admissible number of regressors

K = np.shape(X)[1]

for k in range(K+1):

print("Computing k=%1.0f" % k, end ="")

# Loop over all combinations

for i in combinations(range(K), k):

# Subset X

X_subset = X.iloc[:,list(i)]

# Get dummies for categorical variables

if k>0:

categ_subset = list(categ_cols & set(X_subset.columns))

X_subset = pd.get_dummies(X_subset, columns=categ_subset, drop_first=True)

# Regress

reg = OLS(y,add_constant(X_subset)).fit()

# Metrics

for i,metric in enumerate(args):

score = np.reshape([k,metric(reg)], (1,-1))

scores[i] = np.append(scores[i], score, axis=0)

print("", end="\r")

return scores

We are going to consider 10 variables and two difference metrics: the Sum of Squares Residuals and $R^2$.

# Set metrics

rss = lambda reg : reg.ssr

r2 = lambda reg : reg.rsquared

# Compute scores

scores = model_selection(X, y, rss, r2)

ms_RSS = scores[0]

ms_R2 = scores[1]

Computing k=10

# Save best scores

K = np.shape(X)[1]

ms_RSS_best = [np.min(ms_RSS[ms_RSS[:,0]==k,1]) for k in range(K+1)]

ms_R2_best = [np.max(ms_R2[ms_R2[:,0]==k,1]) for k in range(K+1)]

Let’s plot the best scores.

# Figure 6.1

def make_figure_6_1():

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Figure 6.1: Best Model Selection')

# RSS

ax1.scatter(x=ms_RSS[:,0], y=ms_RSS[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax1.plot(range(K+1), ms_RSS_best, c='r');

ax1.scatter(np.argmin(ms_RSS_best), np.min(ms_RSS_best), marker='x', s=300)

ax1.set_ylabel('RSS');

# R2

ax2.scatter(x=ms_R2[:,0], y=ms_R2[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax2.plot(range(K+1), ms_R2_best, c='r');

ax2.scatter(np.argmax(ms_R2_best), np.max(ms_R2_best), marker='x', s=300)

ax2.set_ylabel('R2');

# All axes;

for ax in fig.axes:

ax.set_xlabel('Number of Predictors');

ax.set_yticks([]);

make_figure_6_1()

The figure shows that, as expected, both metrics improve as the number of variables increases; however, from the three-variable model on, there is little improvement in RSS and $R^2$ as a result of including additional predictors.

Forward Stepwise Selection

For computational reasons, best subset selection cannot be applied with very large $p$.

While the best subset selection procedure considers all $2^p$ possible models containing subsets of the p predictors, forward step-wise considers a much smaller set of models. Forward stepwise selection begins with a model containing no predictors, and then adds predictors to the model, one-at-a-time, until all of the predictors are in the model. In particular, at each step the variable that gives the greatest additional improvement to the fit is added to the model.

def forward_selection(X, y, f):

# Init RSS and R2

K = np.shape(X)[1]

fms_scores = np.zeros((K,1))

# Categorical variables

categ_cols = {"Gender", "Student", "Married", "Ethnicity"}

# Loop over p

selected_cols = []

for k in range(1,K+1):

# Loop over selected columns

remaining_cols = [col for col in X.columns if col not in selected_cols]

temp_scores = np.zeros((0,1))

# Loop on remaining columns

for col in remaining_cols:

# Subset X

X_subset = X.loc[:,selected_cols + [col]]

if k>0:

categ_subset = list(categ_cols & set(X_subset.columns))

X_subset = pd.get_dummies(X_subset, columns=categ_subset, drop_first=True)

# Regress

reg = OLS(y,add_constant(X_subset).values).fit()

# Metrics

temp_scores = np.append(temp_scores, f(reg))

# Pick best variable

best_col = remaining_cols[np.argmin(temp_scores)]

print(best_col)

selected_cols += [best_col]

fms_scores[k-1] = np.min(temp_scores)

return fms_scores

Let’s select the best model according, using the sum of squared residuals as a metric.

What are the most important variables?

# Forward selection by RSS

rss = lambda reg : reg.ssr

fms_RSS = forward_selection(X, y, rss)

Rating

Income

Student

Limit

Cards

Age

Ethnicity

Gender

Married

Education

What happens if we use $R^2$ instead?

# Forward selection by R2

r2 = lambda reg : -reg.rsquared

fms_R2 = -forward_selection(X, y, r2)

Rating

Income

Student

Limit

Cards

Age

Ethnicity

Gender

Married

Education

Unsurprisingly, both methods select the same models. Why? In the end $R^2$ is just a normalized version of RSS.

Let’s plot the scores of the two methods, for different number of predictors.

# New figure 1

def make_new_figure_1():

# Init

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Forward Model Selection')

# RSS

ax1.plot(range(1,K+1), fms_RSS, c='r');

ax1.scatter(np.argmin(fms_RSS)+1, np.min(fms_RSS), marker='x', s=300)

ax1.set_ylabel('RSS');

# R2

ax2.plot(range(1,K+1), fms_R2, c='r');

ax2.scatter(np.argmax(fms_R2)+1, np.max(fms_R2), marker='x', s=300)

ax2.set_ylabel('R2');

# All axes;

for ax in fig.axes:

ax.set_xlabel('Number of Predictors');

ax.set_yticks([]);

make_new_figure_1()

Backward Stepwise Selection

Like forward stepwise selection, backward stepwise selection provides an efficient alternative to best subset selection. However, unlike forward stepwise selection, it begins with the full least squares model containing all p predictors, and then iteratively removes the least useful predictor, one-at-a-time.

def backward_selection(X, y, f):

# Init RSS and R2

K = np.shape(X)[1]

fms_scores = np.zeros((K,1))

# Categorical variables

categ_cols = {"Gender", "Student", "Married", "Ethnicity"}

# Loop over p

selected_cols = list(X.columns)

for k in range(K,0,-1):

# Loop over selected columns

temp_scores = np.zeros((0,1))

# Loop on remaining columns

for col in selected_cols:

# Subset X

X_subset = X.loc[:,[x for x in selected_cols if x != col]]

if k>1:

categ_subset = list(categ_cols & set(X_subset.columns))

X_subset = pd.get_dummies(X_subset, columns=categ_subset, drop_first=True)

# Regress

reg = OLS(y,add_constant(X_subset).values).fit()

# Metrics

temp_scores = np.append(temp_scores, f(reg))

# Pick best variable

worst_col = selected_cols[np.argmin(temp_scores)]

print(worst_col)

selected_cols.remove(worst_col)

fms_scores[k-1] = np.min(temp_scores)

return fms_scores

Let’s select the best model according, using the sum of squared residuals as a metric.

What are the most important variables?

# Backward selection by RSS

rss = lambda reg : reg.ssr

bms_RSS = backward_selection(X, y, rss)

Education

Married

Gender

Ethnicity

Age

Rating

Cards

Student

Income

Limit

What if we use $R^2$ instead?

# Backward selection by R2

r2 = lambda reg : -reg.rsquared

bms_R2 = -backward_selection(X, y, r2)

Education

Married

Gender

Ethnicity

Age

Rating

Cards

Student

Income

Limit

The interesting part here is that the the variable Rating that was selected first by forward model selection, is now dropped $5^{th}$ to last. Why? It’s probably because it contains a lot of information by itself (hence first in FMS) but it’s highly correlated with Student, Income and Limit while these variables are more ortogonal to each other, and hence it gets dropped before them in BMS.

# Plot correlations

sns.pairplot(credit[['Rating','Student','Income','Limit']], height=1.8);

If is indeed what we see: Rating and Limit are highly correlated.

Let’s plot the scores for different number of predictors.

# New figure 2

def make_new_figure_2():

# Init

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Backward Model Selection')

# RSS

ax1.plot(range(1,K+1), bms_RSS, c='r');

ax1.scatter(np.argmin(bms_RSS)+1, np.min(bms_RSS), marker='x', s=300)

ax1.set_ylabel('RSS');

# R2

ax2.plot(range(1,K+1), bms_R2, c='r');

ax2.scatter(np.argmax(bms_R2)+1, np.max(bms_R2), marker='x', s=300)

ax2.set_ylabel('R2');

# All axes;

for ax in fig.axes:

ax.set_xlabel('Number of Predictors');

ax.set_yticks([]);

make_new_figure_2()

Choosing the Optimal Model

So far we have use the trainint error in order to select the model. However, the training error can be a poor estimate of the test error. Therefore, RSS and R2 are not suitable for selecting the best model among a collection of models with different numbers of predictors.

In order to select the best model with respect to test error, we need to estimate this test error. There are two common approaches:

- We can indirectly estimate test error by making an adjustment to the training error to account for the bias due to overfitting.

- We can directly estimate the test error, using either a validation set approach or a cross-validation approach.

Some metrics that account for the trainint error are

- Akaike Information Criterium (AIC)

- Bayesian Information Criterium (BIC)

- Adjusted $R^2$

The idea behind all these varaibles is to insert a penalty for the number of parameters used in the model. All these measure have theoretical fundations which are beyond the scope of this session.

We are now going to test the three metrics

# Set metrics

aic = lambda reg : reg.aic

bic = lambda reg : reg.bic

r2a = lambda reg : reg.rsquared_adj

# Compute best model selection scores

scores = model_selection(X, y, aic, bic, r2a)

ms_AIC = scores[0]

ms_BIC = scores[1]

ms_R2a = scores[2]

Computing k=10

# Save best scores

ms_AIC_best = [np.min(ms_AIC[ms_AIC[:,0]==k,1]) for k in range(K+1)]

ms_BIC_best = [np.min(ms_BIC[ms_BIC[:,0]==k,1]) for k in range(K+1)]

ms_R2a_best = [np.max(ms_R2a[ms_R2a[:,0]==k,1]) for k in range(K+1)]

We plot the scores for different model selection methods.

# Figure 6.2

def make_figure_6_2():

# Init

fig, (ax1,ax2,ax3) = plt.subplots(1,3, figsize=(16,5))

fig.suptitle('Figure 6.2')

# AIC

ax1.scatter(x=ms_AIC[:,0], y=ms_AIC[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax1.plot(range(K+1),ms_AIC_best, c='r');

ax1.scatter(np.argmin(ms_AIC_best), np.min(ms_AIC_best), marker='x', s=300)

ax1.set_ylabel('AIC');

# BIC

ax2.scatter(x=ms_BIC[:,0], y=ms_BIC[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax2.plot(range(K+1), ms_BIC_best, c='r');

ax2.scatter(np.argmin(ms_BIC_best), np.min(ms_BIC_best), marker='x', s=300)

ax2.set_ylabel('BIC');

# R2 adj

ax3.scatter(x=ms_R2a[:,0], y=ms_R2a[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax3.plot(range(K+1), ms_R2a_best, c='r');

ax3.scatter(np.argmax(ms_R2a_best), np.max(ms_R2a_best), marker='x', s=300)

ax3.set_ylabel('R2_adj');

# All axes;

for ax in fig.axes:

ax.set_xlabel('Number of Predictors');

ax.set_yticks([]);

make_figure_6_2()

As we can see, all three metrics select more parsimonious models, with BIC being particularly conservative with only 4 variables and $R^2_{adj}$ selecting the larger model with 7 variables.

Validation and Cross-Validation

As an alternative to the approaches just discussed, we can directly estimate the test error using the validation set and cross-validation methods discussed in the previous session.

The main problem with cross-validation is the computational burden. We are now going to perform best model selection using the following cross-validation algorithms:

- Validation set approach, 50-50 split, repeated 10 times

- 5-fold cross-validation

- 10-fold cross-validation

We are not going to perform Leave-One-Out cross-validation for computational reasons.

def cv_scores(X, y, *args):

# Init

scores = list(itertools.repeat(np.zeros((0,2)), len(args)))

# Categorical variables

categ_cols = {"Gender", "Student", "Married", "Ethnicity"}

# Loop over all possible combinations of regressions

K = np.shape(X)[1]

for k in range(K+1):

print("Computing k=%1.0f" % k, end ="")

for i in combinations(range(K), k):

# Subset X

X_subset = X.iloc[:,list(i)]

# Get dummies for categorical variables

if k>0:

categ_subset = list(categ_cols & set(X_subset.columns))

X_subset = pd.get_dummies(X_subset, columns=categ_subset, drop_first=True)

# Metrics

for i,cv_method in enumerate(args):

score = cross_val_score(LinearRegression(), add_constant(X_subset), y,

cv=cv_method, scoring='neg_mean_squared_error').mean()

score_pair = np.reshape([k,score], (1,-1))

scores[i] = np.append(scores[i], score_pair, axis=0)

print("", end="\r")

return scores

Let’s compute the scores for different model selection methods.

# Define cv methods

vset = ShuffleSplit(n_splits=10, test_size=0.5)

kf5 = KFold(n_splits=5, shuffle=True)

kf10 = KFold(n_splits=10, shuffle=True)

# Get best model selection scores

scores = cv_scores(X, y, vset, kf5, kf10)

ms_vset = scores[0]

ms_kf5 = scores[1]

ms_kf10 = scores[2]

Computing k=10

# Save best scores

ms_vset_best = [np.max(ms_vset[ms_vset[:,0]==k,1]) for k in range(K+1)]

ms_kf5_best = [np.max(ms_kf5[ms_kf5[:,0]==k,1]) for k in range(K+1)]

ms_kf10_best = [np.max(ms_kf10[ms_kf10[:,0]==k,1]) for k in range(K+1)]

We not plot the scores.

# Figure 6.3

def make_figure_6_3():

# Init

fig, (ax1,ax2,ax3) = plt.subplots(1,3, figsize=(16,5))

fig.suptitle('Figure 6.3')

# Validation Set

ax1.scatter(x=ms_vset[:,0], y=ms_vset[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax1.plot(range(K+1),ms_vset_best, c='r');

ax1.scatter(np.argmax(ms_vset_best), np.max(ms_vset_best), marker='x', s=300)

ax1.set_ylabel('Validation Set');

# 5-Fold Cross Validation

ax2.scatter(x=ms_kf5[:,0], y=ms_kf5[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax2.plot(range(K+1), ms_kf5_best, c='r');

ax2.scatter(np.argmax(ms_kf5_best), np.max(ms_kf5_best), marker='x', s=300)

ax2.set_ylabel('5-Fold Cross Validation');

# 10-Fold Cross-Validation

ax3.scatter(x=ms_kf10[:,0], y=ms_kf10[:,1], facecolors='None', edgecolors='k', alpha=0.5);

ax3.plot(range(K+1), ms_kf10_best, c='r');

ax3.scatter(np.argmax(ms_kf10_best), np.max(ms_kf10_best), marker='x', s=300)

ax3.set_ylabel('10-Fold Cross-Validation');

# All axes;

for ax in fig.axes:

ax.set_xlabel('Number of Predictors');

ax.set_yticks([]);

make_figure_6_3()

From the figure we see that each cross-validation method selects a different model and the most accurate one, K-fold CV, select 5 predictors.

5.2 Shrinkage Methods

Model selection methods constrained the number of varaibles before running a linear regression. Shrinkage methods attempt to do the two things simultaneously. In particular they constrain or shrink coefficients by imposing penalties in the objective functions for high values of the parameters.

Ridge Regression

The Least Squares Regression minimizes the Residual Sum of Squares

$$ \mathrm{RSS}=\sum_{i=1}^{n}\left(y_{i}-\beta_{0}-\sum_{j=1}^{p} \beta_{j} x_{i j}\right)^{2} $$

The Ridge Regression objective function instead is

$$ \sum_{i=1}^{n}\left(y_{i}-\beta_{0}-\sum_{j=1}^{p} \beta_{j} x_{i j}\right)^{2}+\lambda \sum_{j=1}^{p} \beta_{j}^{2}=\mathrm{RSS}+\lambda \sum_{j=1}^{p} \beta_{j}^{2} $$

where $\lambda>0$ is a tuning parameter that regulates the extent to which large parameters are penalized.

In matrix notation, the objective function is

$$ ||X\beta - y||^2_2 + \alpha ||\beta||^2_2 $$

which is equivalent to optimizing

$$ \frac{1}{N}||X\beta - y||^2_2 + \frac{\alpha}{N} ||\beta||^2_2 $$

We are now going to run Ridge Regression on the Credit dataset trying to explain account Balance with a set of observable individual characteristics.

# X and y

categ_cols = ["Gender", "Student", "Married", "Ethnicity"]

X = credit.loc[:, credit.columns != 'Balance']

X = pd.get_dummies(X, columns=categ_cols, drop_first=True)

y = credit.loc[:,'Balance']

n = len(credit)

We run ridge regression over a range of values for the penalty paramenter $\lambda$.

# Init alpha grid

n_grid = 100

alphas = 10**np.linspace(-2,5,n_grid).reshape(-1,1)

ridge = Ridge()

ridge_coefs = []

# Loop over values of alpha

for a in alphas:

ridge.set_params(alpha=a)

ridge.fit(scale(X), y)

ridge_coefs.append(ridge.coef_)

ridge_coefs = np.reshape(ridge_coefs,(n_grid,-1))

We use linear regression as a comparison.

# OLS regression

ols = LinearRegression().fit(scale(X),y)

ols_coefs = ols.coef_;

mod_ols = np.linalg.norm(ols_coefs)

# Relative magnitude

rel_beta = [np.linalg.norm(ridge_coefs[k,:])/mod_ols for k in range(n_grid)]

rel_beta = np.reshape(rel_beta, (-1,1))

We plot the results

# Figure 6.4

def make_figure_6_4():

# Init

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Figure 6.4: Ridge Regression Coefficients')

highlight = [0,1,2,7];

# Plot coefficients - absolute

ax1.plot(alphas, ridge_coefs[:,highlight], alpha=1)

ax1.plot(alphas, ridge_coefs, c='grey', alpha=0.3)

ax1.set_xscale('log')

ax1.set_xlabel('lambda'); ax1.set_ylabel('Standardized coefficients');

ax1.legend(['Income', 'Limit', 'Rating', 'Student'])

# Plot coefficients - relative

ax2.plot(rel_beta, ridge_coefs[:,highlight], alpha=1)

ax2.plot(rel_beta, ridge_coefs, c='grey', alpha=0.3)

ax2.set_xlabel('Relative Beta'); ax2.set_ylabel('Standardized coefficients');

make_figure_6_4()

As we decrease $\lambda$, the Ridge coefficients get larger. Moreover, the variables with the consistently largest coefficients are Income, Limit, Rating and Student.

Bias-Variance Trade-off

Ridge regression’s advantage over least squares is rooted in the bias-variance trade-off. As $\lambda$ increases, the flexibility of the ridge regression fit decreases, leading to decreased variance but increased bias.

$$ y_0 = f(x_0) + \varepsilon $$

Recap: we can decompose the Mean Squared Error of an estimator into two components: the variance and the squared bias:

$$ \mathbb E\left(y_{0}-\hat{f}\left(x_{0}\right)\right)^{2} = \mathbb E\left(f(x_0) + \varepsilon - \hat f(x_{0})\right)^{2} = \ = \mathbb E\left(f(x_0) - \mathbb E[\hat f(x_{0})] + \varepsilon - \hat f(x_{0}) + \mathbb E[\hat f(x_{0})] \right)^{2} = \ = \mathbb E \left[ \mathbb E [\hat{f} (x_{0}) ] - f(x_0) \right]^2 + \mathbb E \left[ \left( \hat{f} (x_{0}) - \mathbb E [\hat{f} (x_{0})] \right)^2 \right] + \mathbb E[\varepsilon^2] \ = \operatorname{Bias} \left( \hat{f} (x_{0}) \right)^2 + \operatorname{Var}\left(\hat{f}\left(x_{0}\right)\right) + \operatorname{Var}(\varepsilon) $$

The last term is the variance of the error term, sometimes also called the irreducible error since it’s pure noise, and we cannot account for it.

# Compute var-bias

def compute_var_bias(X_train, b0, x0, a, k, n, sim, f):

# Init

y_hat = np.zeros(sim)

coefs = np.zeros((sim, k))

# Loop over simulations

for s in range(sim):

e_train = normal(0,1,(n,1))

y_train = X_train @ b0 + e_train

fit = f(a).fit(X_train, y_train)

y_hat[s] = fit.predict(x0)

coefs[s,:] = fit.coef_

# Compute MSE, Var and Bias2

e_test = normal(0,1,(sim,1))

y_test = x0 @ b0 + e_test

mse = np.mean((y_test - y_hat)**2)

var = np.var(y_hat)

bias2 = np.mean(x0 @ b0 - y_hat)**2

return [mse, var, bias2], np.mean(coefs, axis=0)

np.random.seed(1)

# Generate random data

n = 50

k = 45

N = 50000

X_train = normal(0.2,1,(n,k))

x0 = normal(0.2,1,(1,k))

e_train = normal(0,1,(n,1))

b0 = uniform(0,1,(k,1))

# Init alpha grid

sim = 1000

n_grid = 30

df = pd.DataFrame({'alpha':10**np.linspace(-5,5,n_grid)})

ridge_coefs2 = []

# Init simulations

sim = 1000

ridge = lambda a: Ridge(alpha=a, fit_intercept=False)

# Loop over values of alpha

for i in range(len(df)):

print("Alpha %1.0f/%1.0f" % (i+1,len(df)), end ="")

a = df.loc[i,'alpha']

df.loc[i,['mse','var','bias2']], c = compute_var_bias(X_train, b0, x0, a, k, n, sim, ridge)

ridge_coefs2.append(c)

print("", end="\r")

ridge_coefs2 = np.reshape(ridge_coefs2,(n_grid,-1))

Alpha 30/30

# OLS regression

y_train = X_train @ b0 + e_train

ols = LinearRegression().fit(X_train,y_train)

ols_coefs = ols.coef_;

mod_ols = np.linalg.norm(ols_coefs)

# Relative magnitude

rel_beta = [np.linalg.norm(ridge_coefs2[i,:])/mod_ols for i in range(n_grid)]

rel_beta = np.reshape(rel_beta, (-1,1))

# Figure 6.5

def make_figure_6_5():

# Init

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Figure 6.5: Ridge Bias-Var decomposition')

# MSE

ax1.plot(df['alpha'], df[['bias2','var','mse']]);

ax1.set_xscale('log');

ax1.set_xlabel('lambda'); ax1.set_ylabel('Mean Squared Error');

ax1.legend(['Bias2','Variance','MSE'], fontsize=12);

# MSE

ax2.plot(rel_beta, df[['bias2','var','mse']]);

ax2.set_xlabel('Relative Beta'); ax2.set_ylabel('Mean Squared Error');

ax2.legend(['Bias2','Variance','MSE'], fontsize=12);

make_figure_6_5()

Ridge regression has the advantage of shrinking coefficients. However, unlike best subset, forward stepwise, and backward stepwise selection, which will generally select models that involve just a subset of the variables, ridge regression will include all $p$ predictors in the final model.

Lasso solves that problem by using a different penalty function.

Lasso

The lasso coefficients minimize the following objective function:

$$ \sum_{i=1}^{n}\left(y_{i}-\beta_{0}-\sum_{j=1}^{p} \beta_{j} x_{i j}\right)^{2}+\lambda \sum_{j=1}^{p}\left|\beta_{j}\right| = \mathrm{RSS} + \lambda \sum_{j=1}^p|\beta_j| $$

so that the main difference with respect to ridge regression is the penalty function $\lambda \sum_{j=1}^{p}\left|\beta_{j}\right|$ instead of $\lambda \sum_{j=1}^p (\beta_j)^2$.

A consequence of this objective function is that Lasso is much more likely to shrink coefficients to exactly zero, while Ridge only decreases their magnitude. The reason why lies in the shape of the objective function. You can rewrite the Ridge and Lasso minimization problems as constrained optimization:

-

Ridge $$ \underset{\beta}{\operatorname{min}} \ \left{\sum_{i=1}^{n}\left(y_{i}-\beta_{0}-\sum_{j=1}^{p} \beta_{j} x_{i j}\right)^{2}\right} \quad \text { subject to } \quad \sum_{j=1}^{p}\left|\beta_{j}\right| \leq s $$

-

Lasso $$ \underset{\beta}{\operatorname{min}} \ \left{\sum_{i=1}^{n}\left(y_{i}-\beta_{0}-\sum_{j=1}^{p} \beta_{j} x_{i j}\right)^{2}\right} \quad \text { subject to } \quad \sum_{j=1}^{p} \beta_{j}^{2} \leq s $$

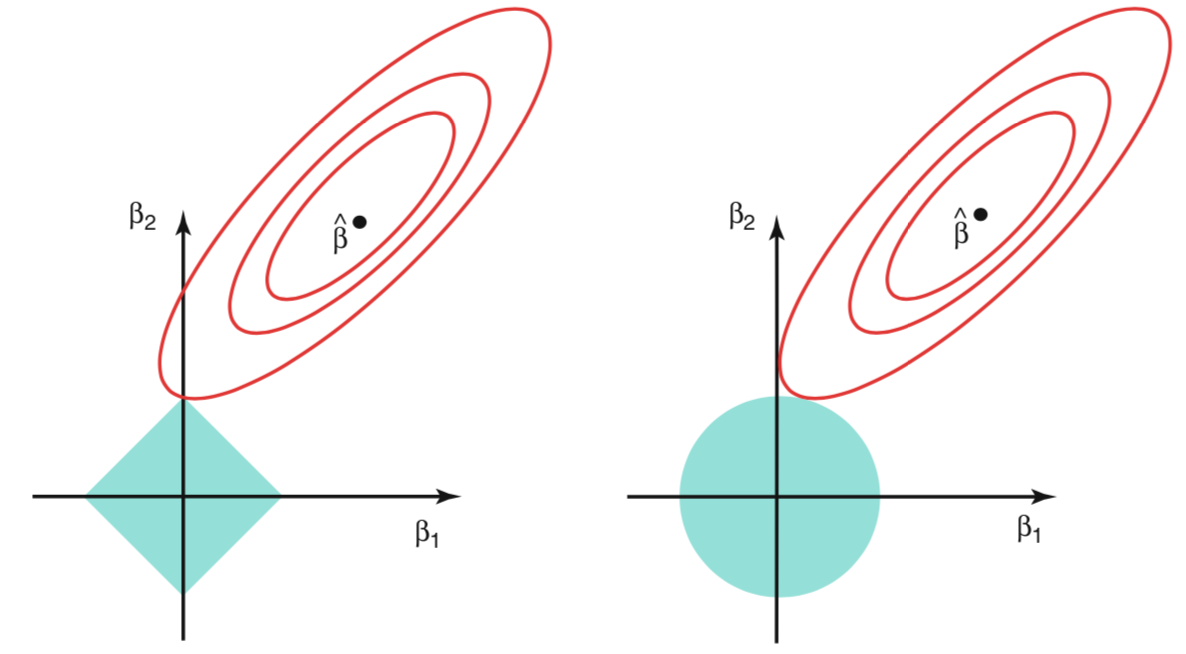

In pictures, constrained optimization problem lookes like this.

The red curves represents the contour sets of the RSS. They are elliptical since the objective function is quadratic. The blue area represents the admissible set, i.e. the constraints. As we can see, it is much easier with Lasso to have the constrained optimum on one of the edges of the rhombus.

We are now going to repeat the same exercise on the Credit dataset, trying to predict account Balance with a set of obsevable induvidual characteristics, for different values of the penalty paramenter $\lambda$.

# X and y

categ_cols = ["Gender", "Student", "Married", "Ethnicity"]

X = credit.loc[:, credit.columns != 'Balance']

X = pd.get_dummies(X, columns=categ_cols, drop_first=True)

y = credit.loc[:,'Balance']

The $\lambda$ grid is going to be slightly different now.

# Init alpha grid

n_grid = 100

alphas = 10**np.linspace(0,3,n_grid).reshape(-1,1)

lasso = Lasso()

lasso_coefs = []

# Loop over values of alpha

for a in alphas:

lasso.set_params(alpha=a)

lasso.fit(scale(X), y)

lasso_coefs.append(lasso.coef_)

lasso_coefs = np.reshape(lasso_coefs,(n_grid,-1))

We run OLS to plot the relative magnitude of the Lasso coefficients.

# Relative magnitude

mod_ols = np.linalg.norm(ols_coefs)

rel_beta = [np.linalg.norm(lasso_coefs[i,:])/mod_ols for i in range(n_grid)]

rel_beta = np.reshape(rel_beta, (-1,1))

We plot the magnitude of the coefficients $\beta$

- for different values of $\lambda$

- for different values of of $||\beta||$

# Figure 6.6

def make_figure_6_6():

# Init

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Figure 6.6')

highlight = [0,1,2,7];

# Plot coefficients - absolute

ax1.plot(alphas, lasso_coefs[:,highlight], alpha=1)

ax1.plot(alphas, lasso_coefs, c='grey', alpha=0.3)

ax1.set_xscale('log')

ax1.set_xlabel('lambda'); ax1.set_ylabel('Standardized coefficients');

ax1.legend(['Income', 'Limit', 'Rating', 'Student'], fontsize=12)

# Plot coefficients - relative

ax2.plot(rel_beta, lasso_coefs[:,highlight], alpha=1)

ax2.plot(rel_beta, lasso_coefs, c='grey', alpha=0.3)

ax2.set_xlabel('relative mod beta'); ax2.set_ylabel('Standardized coefficients');

make_figure_6_6()

Rating seems to be the most important variable, followed by Limit and Student.

As with ridge regression, the lasso shrinks the coefficient estimates towards zero. However, in the case of the lasso, the $l_1$ penalty has the effect of forcing some of the coefficient estimates to be exactly equal to zero when the tuning parameter $\lambda$ is sufficiently large. Hence, much like best subset selection, the lasso performs variable selection.

We say that the lasso yields sparse models — that is, models that involve only a subset of the variable

We now plot how the choice of $\lambda$ affects the bias-variance trade-off.

# Init alpha grid

sim = 1000

n_grid = 30

df = pd.DataFrame({'alpha':10**np.linspace(-1,1,n_grid)})

lasso_coefs2 = []

# Init simulations

sim = 1000

lasso = lambda a: Lasso(alpha=a, fit_intercept=False)

# Loop over values of alpha

for i in range(len(df)):

print("Alpha %1.0f/%1.0f" % (i+1,len(df)), end ="")

a = df.loc[i,'alpha']

df.loc[i,['mse','var','bias2']], c = compute_var_bias(X_train, b0, x0, a, k, n, sim, lasso)

lasso_coefs2.append(c)

print("", end="\r")

lasso_coefs2 = np.reshape(lasso_coefs2,(n_grid,-1))

Alpha 30/30

# Relative magnitude

mod_ols = np.linalg.norm(ols_coefs)

rel_beta = [np.linalg.norm(lasso_coefs2[k,:])/mod_ols for k in range(n_grid)]

rel_beta = np.reshape(rel_beta, (-1,1))

# OLS regression

y_train = X_train @ b0 + e_train

ols = LinearRegression().fit(X_train,y_train)

ols_coefs = ols.coef_;

mod_ols = np.linalg.norm(ols_coefs)

# Relative magnitude

mod_ols = np.linalg.norm(ols_coefs)

rel_beta = [np.linalg.norm(lasso_coefs2[k,:])/mod_ols for k in range(n_grid)]

rel_beta = np.reshape(rel_beta, (-1,1))

# Figure 6.8

def make_figure_6_8():

fig, (ax1,ax2) = plt.subplots(1,2, figsize=(12,5))

fig.suptitle('Figure 6.8: Lasso Bias-Var decomposition')

# MSE

ax1.plot(df['alpha'], df[['bias2','var','mse']]);

ax1.set_xscale('log');

ax1.set_xlabel('lambda'); ax1.set_ylabel('Mean Squared Error');

ax1.legend(['Bias2','Variance','MSE'], fontsize=12);

# MSE

ax2.plot(rel_beta, df[['bias2','var','mse']]);

ax2.set_xlabel('Relative Beta'); ax1.set_ylabel('Mean Squared Error');

ax2.legend(['Bias2','Variance','MSE'], fontsize=12);

make_figure_6_8()

As $\lambda$ increases the squared bias increases and the variance decreases.

Comparing the Lasso and Ridge Regression

In order to obtain a better intuition about the behavior of ridge regression and the lasso, consider a simple special case with $n = p$, and $X$ a diagonal matrix with $1$’s on the diagonal and $0$’s in all off-diagonal elements. To simplify the problem further, assume also that we are performing regression without an intercept.

With these assumptions, the usual least squares problem simplifies to the coefficients that minimize

$$ \sum_{j=1}^{p}\left(y_{j}-\beta_{j}\right)^{2} $$

In this case, the least squares solution is given by

$$ \hat \beta_j = y_j $$

One can show that in this setting, the ridge regression estimates take the form

$$ \hat \beta_j^{RIDGE} = \frac{y_j}{1+\lambda} $$

and the lasso estimates take the form

$$ \hat{\beta}{j}^{LASSO}=\left{\begin{array}{ll} y{j}-\lambda / 2 & \text { if } y_{j}>\lambda / 2 \ y_{j}+\lambda / 2 & \text { if } y_{j}<-\lambda / 2 \ 0 & \text { if }\left|y_{j}\right| \leq \lambda / 2 \end{array}\right. $$

We plot the relationship visually.

np.random.seed(3)

# Generate random data

n = 100

k = n

X = np.eye(k)

e = normal(0,1,(n,1))

b0 = uniform(-1,1,(k,1))

y = X @ b0 + e

# OLS regression

reg = LinearRegression().fit(X,y)

ols_coefs = reg.coef_;

# Ridge regression

ridge = Ridge(alpha=1).fit(X,y)

ridge_coefs = ridge.coef_;

# Ridge regression

lasso = Lasso(alpha=0.01).fit(X,y)

lasso_coefs = lasso.coef_.reshape(1,-1);

# sort

order = np.argsort(y.reshape(1,-1), axis=1)

y_sorted = np.take_along_axis(ols_coefs, order, axis=1)

ols_coefs = np.take_along_axis(ols_coefs, order, axis=1)

ridge_coefs = np.take_along_axis(ridge_coefs, order, axis=1)

lasso_coefs = np.take_along_axis(lasso_coefs, order, axis=1)

# Figure 6.10

def make_figure_6_10():

# Init

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Figure 6.10')

# Ridge

ax1.plot(y_sorted.T, ols_coefs.T)

ax1.plot(y_sorted.T, ridge_coefs.T)

ax1.set_xlabel('True Coefficient'); ax1.set_ylabel('Estimated Coefficient');

ax1.legend(['OLS','Ridge'], fontsize=12);

# Lasso

ax2.plot(y_sorted.T, ols_coefs.T)

ax2.plot(y_sorted.T, lasso_coefs.T)

ax2.set_xlabel('True Coefficient'); ax2.set_ylabel('Estimated Coefficient');

ax2.legend(['OLS','Lasso'], fontsize=12);

make_figure_6_10()

We see that ridge regression shrinks every dimension of the data by the same proportion, whereas the lasso hrinks all coefficients toward zero by a similar amount, and sufficiently small coefficients are shrunken all the way to zero.

Selecting the Tuning Parameter

Implementing ridge regression and the lasso requires a method for selecting a value for the tuning parameter $\lambda$.

Cross-validation provides a simple way to tackle this problem. We choose a grid of $\lambda$ values, and compute the cross-validation error for each value of $\lambda$. We then select the tuning parameter value for which the cross-validation error is smallest. Finally, the model is re-fit using all of the available observations and the selected value of the tuning parameter.

# X and y

categ_cols = ["Gender", "Student", "Married", "Ethnicity"]

X = credit.loc[:, credit.columns != 'Balance']

X = pd.get_dummies(X, columns=categ_cols, drop_first=True).values

y = credit.loc[:,'Balance']

n = len(credit)

We are going to use 10-fold CV as cross-validation algorithm.

# Get MSE

def cv_lasso(X,y,a):

# Init mse

mse = []

# Generate splits

kf10 = KFold(n_splits=10, random_state=None, shuffle=False)

kf10.get_n_splits(X)

# Loop over splits

for train_index, test_index in kf10.split(X):

X_train, X_test = X[train_index], X[test_index]

y_train, y_test = y[train_index], y[test_index]

lasso = Lasso(alpha=a).fit(X_train, y_train)

y_hat = lasso.predict(X_test)

mse.append(mean_squared_error(y_test, y_hat))

return np.mean(mse)

# Compute MSE over grid of alphas

n_grid = 30

alphas = 10**np.linspace(0,3,n_grid).reshape(-1,1)

MSE = [cv_lasso(X,y,a) for a in alphas]

What is the optimal $\lambda$?

# Find minimum alpha

alpha_min = alphas[np.argmin(MSE)]

print('Best alpha by 10fold CV:',alpha_min[0])

Best alpha by 10fold CV: 2.592943797404667

We now plot the objective function and the implied coefficients at the optimal $\lambda$.

# Get coefficients

coefs = []

# Loop over values of alpha

for a in alphas:

lasso = Lasso(alpha=a).fit(scale(X), y)

coefs.append(lasso.coef_)

coefs = np.reshape(coefs,(n_grid,-1))

np.shape(coefs)

(30, 11)

# Figure 6.12

def make_figure_6_12():

# Init

fig, (ax1,ax2) = plt.subplots(1,2)

fig.suptitle('Figure 6.12: Lasso 10-fold CV')

# MSE by LOO CV

ax1.plot(alphas, MSE, alpha=1);

ax1.axvline(alpha_min, c='k', ls='--')

ax1.set_xscale('log')

ax1.set_xlabel('lambda'); ax1.set_ylabel('MSE');

highlight = [0,1,2,7];

# Plot coefficients - absolute

ax2.plot(alphas, coefs[:,highlight], alpha=1)

ax2.plot(alphas, coefs, c='grey', alpha=0.3)

ax2.axvline(alpha_min, c='k', ls='--')

ax2.set_xscale('log')

ax2.set_xlabel('lambda'); ax2.set_ylabel('Standardized coefficients');

ax2.legend(['Income', 'Limit', 'Rating', 'Student'], fontsize=10);

make_figure_6_12()