Machine Learning Pipeline

Last updated on Mar 30, 2022

In this notebook, we are going to build a pipeline for a general prediction problem.

# Standard Imports

from src.utils import *

from src.get_feature_names import get_feature_names

# Set inline graphs

sns.set()

%matplotlib inline

Introduction

Usually, in machine learning prediction tasks, the data consists in 3 files:

- X_train.csv

- y_train.csv

- X_test.csv

The purpose of the exercise is to produce a y_test.csv file, with the predicted values corresponding to the X_test.csv observations.

The functions we will write are going to be general and will adapt to any type of dataset, and we will test them on the House Prices Dataset which is a standard dataset for these kind of tasks. The data consists of 2 files:

- train.csv

- test.csv

The target variable that we want to predict is SalePrice.

Setup

First we want to import the data.

# Import data

df_train = pd.read_csv("data/train.csv")

df_test = pd.read_csv("data/test.csv")

print(f"Training data: {np.shape(df_train)} \n Testing data: {np.shape(df_test)}")

Training data: (1460, 81)

Testing data: (1459, 80)

The training data also includes the target variable SalePrice, while, as usual, the testing data does not. We need to separate the training data into two parts:

X: the featuresy: the target

# Select the features

X_train = df_train.drop(['SalePrice'], axis=1)

X_test = df_test

# Check size

print(f"Training features: {np.shape(X_train)} \n Testing features: {np.shape(X_test)}")

Training features: (1460, 80)

Testing features: (1459, 80)

# Select the target

y_train = df_train['SalePrice']

# Check size

print(f"Training target: {np.shape(y_train)}")

Training target: (1460,)

It’s good practice to immediately set aside a validation sample with 20% of the observations. The purpose of the validation sample is to give us unbiased estimate of the prediction score. Therefore, we want to set it aside as soon as possible, not to be conditioned in any way by it. Possibly, set it away even before data exploration.

The more we tune the algorithm based on the feedback received from the validation sample, the more biased our estimate is going to be. Ideally, one would use only cross-validation on the training data and tune only a couple of times using the validation data.

# Set aside the validation sample

X_train, X_validation, y_train, y_validation = train_test_split(X_train, y_train, test_size=0.2)

Now we are ready to build and test our pipeline.

Data Exploration

First, let’s have a quick look at the data.

X_train.head()

| Id | MSSubClass | MSZoning | LotFrontage | LotArea | Street | Alley | LotShape | LandContour | Utilities | ... | ScreenPorch | PoolArea | PoolQC | Fence | MiscFeature | MiscVal | MoSold | YrSold | SaleType | SaleCondition | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 563 | 564 | 50 | RL | 66.0 | 21780 | Pave | NaN | Reg | Lvl | AllPub | ... | 144 | 0 | NaN | NaN | NaN | 0 | 7 | 2008 | WD | Normal |

| 48 | 49 | 190 | RM | 33.0 | 4456 | Pave | NaN | Reg | Lvl | AllPub | ... | 0 | 0 | NaN | NaN | NaN | 0 | 6 | 2009 | New | Partial |

| 148 | 149 | 20 | RL | 63.0 | 7500 | Pave | NaN | Reg | Lvl | AllPub | ... | 0 | 0 | NaN | NaN | NaN | 0 | 4 | 2008 | WD | Normal |

| 801 | 802 | 30 | RM | 40.0 | 4800 | Pave | NaN | Reg | Lvl | AllPub | ... | 0 | 0 | NaN | NaN | NaN | 0 | 7 | 2007 | WD | Normal |

| 1374 | 1375 | 60 | FV | 85.0 | 10625 | Pave | NaN | Reg | Lvl | AllPub | ... | 0 | 0 | NaN | NaN | NaN | 0 | 7 | 2008 | WD | Normal |

5 rows × 80 columns

The Id column is clearly not useful for prediction, let’s drop it from both datasets.

# Drop Id

X_train.drop(["Id"], axis=1, inplace=True)

X_test.drop(["Id"], axis=1, inplace=True)

Now we want to identify categorical and numerical variables.

# Save column types

numerical_cols = list(X_train.describe().columns)

categorical_cols = list(X_train.describe(include=object).columns)

print("There are %i numerical and %i categorical variables" % (len(numerical_cols), len(categorical_cols)))

There are 36 numerical and 43 categorical variables

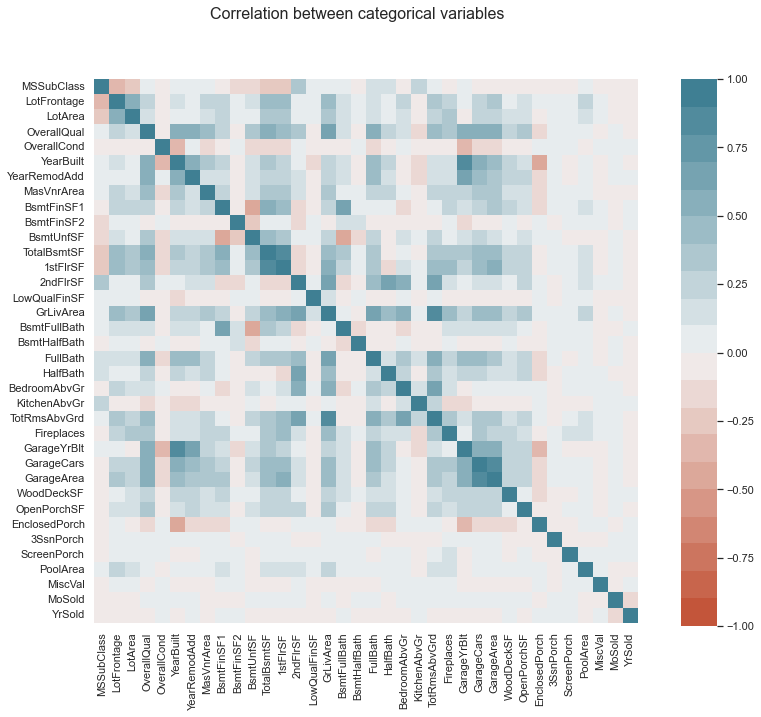

Let’s start by analyzing the numerical variables.

X_numerical = X_train.loc[:, numerical_cols]

corr = X_numerical.corr()

fig, ax = plt.subplots(1, 1, figsize=(10,10))

fig.suptitle("Correlation between categorical variables", fontsize=16)

cbar_ax = fig.add_axes([.95, .12, .05, .76])

sns.heatmap(corr, vmin=-1, vmax=1, center=0, cmap=sns.diverging_palette(20, 220, n=20),

square=True, ax=ax, cbar_ax = cbar_ax)

plt.show()

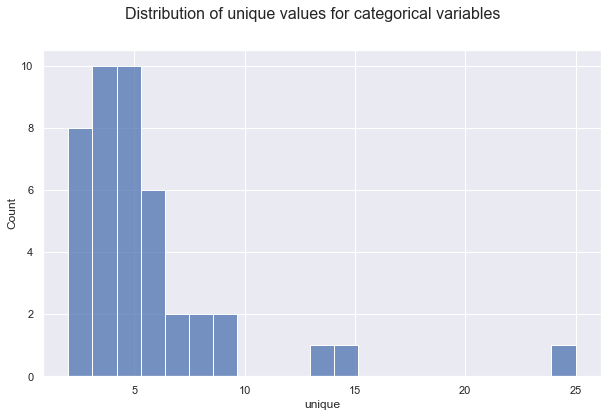

For the non/numeric columns, we need a further option.

unique_values = X_train.describe(include=object).T.unique

# Plot

fig, ax = plt.subplots(1, 1, figsize=(10,6))

fig.suptitle("Distribution of unique values for categorical variables", fontsize=16)

sns.histplot(data=unique_values)

plt.show();

Let’s save the identity of the numerical and categorical columns.

# Save column types

numerical_cols = list(X_train.describe().columns)

categorical_cols = list(X_train.describe(include=object).columns)

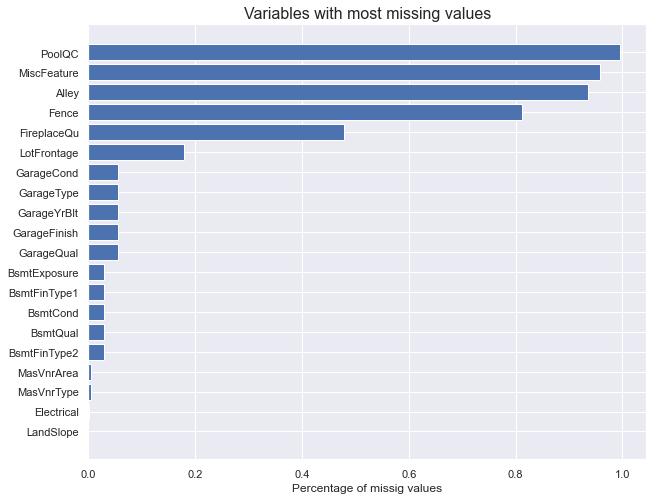

How many missing values are there in the dataset?

missing_values = X_train.isnull().sum().sort_values(ascending=True)[-20:] / len(X_train)

fig, ax = plt.subplots(figsize=(10,8))

ax.set_title("Variables with most missing values", fontsize=16)

ax.barh(np.arange(len(missing_values)), missing_values)

ax.set_yticks(np.arange(len(missing_values)))

ax.set_yticklabels(missing_values.index)

ax.set_xlabel('Percentage of missig values')

plt.show()

Around 10% of each feature is missing. We will have to deal with that.

Pre-processing

First, let’s process numerical variables. We want to do two things:

- inpute missing values

- standardize all variables

Which imputer should to use? It depends on the type of missing data:

-

Missing absolutely at random: as the name says, in this case we believe that missing values are distributed uniformly at random, independently across variables.

- In this case, the only information on missing values comes from the distribution of non-missing values of the same variable.

- No information on missing values is contained in other variables.

-

Missing at random: in this case, missing values are random, conditional on values of other observed variables.

- In this case, information in other variables might help filling missing values.

-

Missing non at random: in this last case, missing values depend on information that we do not observe.

- This is the most tricky category of missing values since data alone does not tell us which values might be missing. For example, we might have that older women might be less likely to report the age.

- If we consider the data missing at random (absolutely or not), we would underestimate the missing ages.

- External information such as the sample population might help. For example, we could estimate the probability of not reporting the age and fill the missing values with the expected age, conditional on age not being reported.

So, which imputers are readily available in sklearn for numerical data?

For data missing absolutely at random, there is one standard sklearn library: SimpleImputer(). It allows different strategy options such as

"mean""median""most_frequent"

For data missing at random, there are multiple sklearn libraries:

KNNImputer(): uses KNNIterativeImputer(): uses a variety of ML algorithms- see comparison here

After we have inputed missing values, we want to standardize numerical variables to make the algorithm more efficient and robust to outliers.

The two main options for standardization are:

StandardScaler(): which normalizes each variable to mean zero and unit varianceMinMaxScaler(): which normalizes each variable to an interval between zero an one

# Inputer for numerical variables

num = Pipeline(steps=[

('ii', IterativeImputer()),

('ss', StandardScaler())

])

For categorical variables, we do not have to worry about scaling. However, we still need to impute missing values and, crucially, we need to transform them into numerical variables. This process is called encoding.

Which imputer should to use?

For data missing absolutely at random, the only available strategy option for SimpleImputer() is

"most_frequent"

For data missing at random, we can still use both

KNNImputer()IterativeImputer()

For encoding categorical variables, the standard option is OneHotEncoder() which generates unique binary variables out of every values of the categorical variable.

# One Hot Encoder for categorical data

cat = Pipeline(steps=[

('si', SimpleImputer(strategy="most_frequent")),

('ohe', OneHotEncoder(handle_unknown="ignore")),

])

# Preprocess column transformer for preprocessing data

preprocess = ColumnTransformer(

transformers=[

('num', num, numerical_cols),

('cat', cat, categorical_cols),

])

Information and components

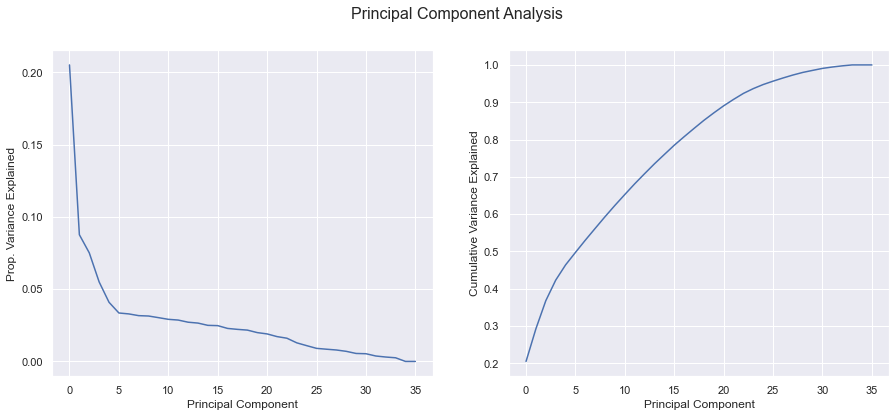

How much information is contained in our dataset? It is a dense or sparse dataset?

X_clean = num.fit_transform(X_numerical)

pca = PCA().fit(X_clean)

explained_variance = pca.explained_variance_ratio_

fig, (ax1, ax2) = plt.subplots(1,2, figsize=(15,6))

fig.suptitle('Principal Component Analysis', fontsize=16);

# Relative

ax1.plot(range(len(explained_variance)), explained_variance)

ax1.set_ylabel('Prop. Variance Explained')

ax1.set_xlabel('Principal Component');

# Cumulative

ax2.plot(range(len(explained_variance)), np.cumsum(explained_variance))

ax2.set_ylabel('Cumulative Variance Explained');

ax2.set_xlabel('Principal Component');

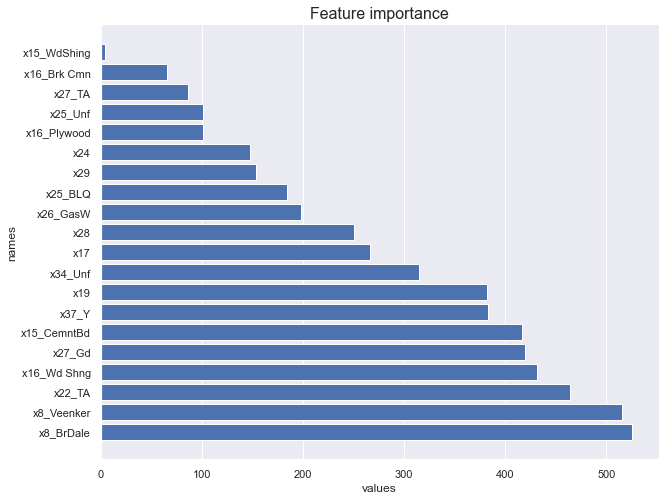

Feature Importance

Before starting our prediction analysis, we would like to understand which variables are most important for our prediction problem.

def plot_featureimportance(importance, preprocess):

df = pd.DataFrame({"names": get_feature_names(preprocess), "values": importance})

df = df.sort_values("values").iloc[:20, :]

# plot

fig, ax = plt.subplots(figsize=(10,8))

ax.set_title("Feature importance", fontsize=16)

sns.barplot(y="names", x="values", data=df)

ax.barh(np.arange(len(df)), df["values"])

plt.show()

We start with linear regression feature importance: we standardize all variables to be mean vero and unit variance, and we run a linear regression over the test set.

def featureimportance_lr(X, y):

X_clean = preprocess.fit_transform(X)

# fit the model

model = LinearRegression()

model.fit(X_clean, y)

# get importance

importance = np.abs(model.coef_)

plot_featureimportance(importance, preprocess)

# Plot linear feature importance

featureimportance_lr(X_train, y_train)

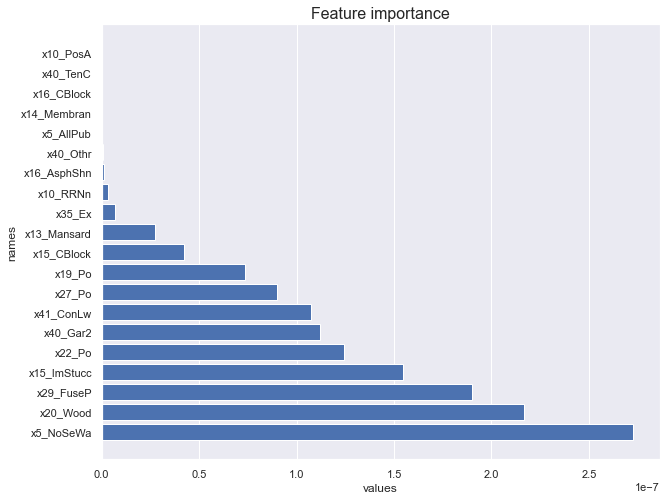

We now look at regression tree feature importance.

def featureimportance_forest(X, y):

X_clean = preprocess.fit_transform(X)

# fit the model

model = RandomForestRegressor()

model.fit(X_clean, y)

# get importance

importance = model.feature_importances_

plot_featureimportance(importance, preprocess)

# Plot tree feature importance

featureimportance_forest(X_train, y_train)

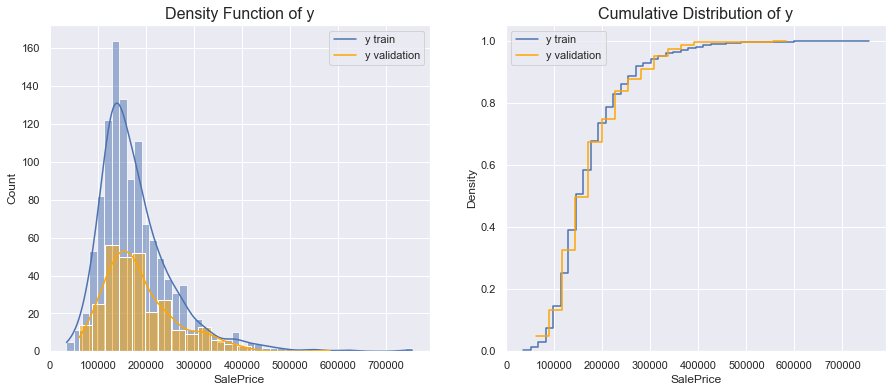

Weighting

Another important check to perform concerns weighting. Is the distribution of our objective variable the same in the training and in the test sample? If it is not the case, we might get a poor performance just because our training sample is not representative of our testing sample.

This is something that usually we cannot test, since we do not have access to the distribution of the target variable in the test data. However, we might be given the information ex-ante as a warning.

In this case, we perform the analysis on the validation set. Since we have selected the validation set at random, we do not expect significant differences.

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15,6))

# Plot 1

sns.histplot(data=y_train, kde=True, ax=ax1)

sns.histplot(data=y_validation, kde=True, ax=ax1, color='orange')

ax1.set_title("Density Function of y", fontsize=16);

ax1.legend(['y train', 'y validation'])

# Plot 2

sns.histplot(data=y_train, element="step", fill=False,

cumulative=True, stat="density", common_norm=False, ax=ax2)

sns.histplot(data=y_validation, element="step", fill=False,

cumulative=True, stat="density", common_norm=False, ax=ax2, color='orange')

ax2.set_title("Cumulative Distribution of y", fontsize=16);

ax2.legend(['y train', 'y validation']);

Since the size of the test sample is smaller than the size of the training sample, the two densities are different. However, the distributions indicate that the standardized distributions are the same.

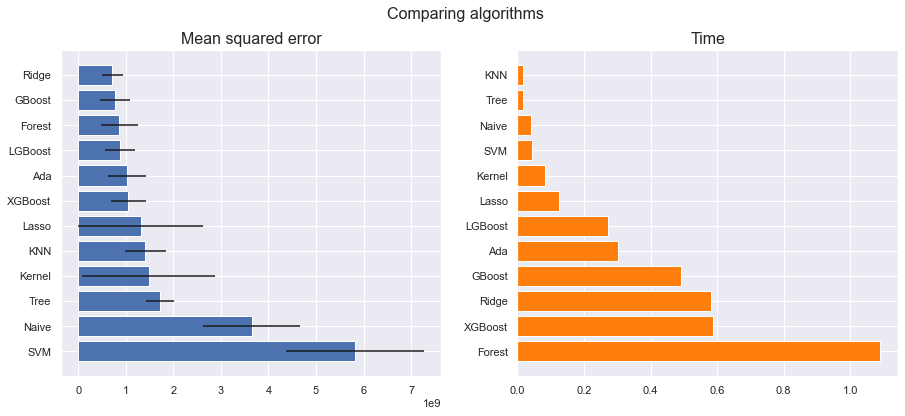

Model

There are many models to choose among.

# prepare models

models = {"Lasso": Lasso(alpha=100),

"Ridge": BayesianRidge(),

"KNN": KNeighborsRegressor(),

"Kernel": KernelRidge(),

"Naive": GaussianNB(),

"SVM": SVR(),

"Ada": AdaBoostRegressor(),

"Tree": DecisionTreeRegressor(),

"Forest": RandomForestRegressor(),

"GBoost": GradientBoostingRegressor(),

"XGBoost": XGBRegressor(),

"LGBoost": LGBMRegressor()}

def evaluate_model(model, name, X, y, cv, scoring):

X_clean = preprocess.fit_transform(X)

start = time.perf_counter()

cv_results = cross_val_score(model, X_clean, y, cv=cv, scoring=scoring)

t = time.perf_counter()-start

score = {"model":name, "mean":-np.mean(cv_results), "std":np.std(cv_results), "time":t}

print("%s: %f (%f) in %f seconds" % (name, -np.mean(cv_results), np.std(cv_results), t))

return score

def plot_model_scores(scores):

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15,6))

fig.suptitle("Comparing algorithms", fontsize=16)

# Plot 1

scores.sort_values("mean", ascending=False, inplace=True)

ax1.set_title("Mean squared error", fontsize=16)

ax1.barh(range(len(scores)), scores["mean"], xerr=scores["std"])

ax1.set_yticks(range(len(scores)))

ax1.set_yticklabels([s for s in scores["model"]])

# Plot 2

scores.sort_values("time", ascending=False, inplace=True)

ax2.set_title("Time", fontsize=16)

ax2.barh(range(len(scores)), scores["time"], color='tab:orange')

ax2.set_yticks(range(len(scores)))

ax2.set_yticklabels([s for s in scores["model"]])

plt.show()

def compare_models(models):

scores = pd.DataFrame()

cv = KFold(n_splits=5)

scoring = 'neg_mean_squared_error'

for name, model in models.items():

score = evaluate_model(model, name, X_validation, y_validation, cv, scoring)

scores = scores.append(score, ignore_index=True)

return scores

scores = compare_models(models)

Lasso: 1309794414.859426 (1313338809.546610) in 0.126276 seconds

Ridge: 715278312.108788 (217652788.836596) in 0.582577 seconds

KNN: 1413048071.753012 (430146510.332671) in 0.016970 seconds

Kernel: 1477920100.374237 (1401354461.497433) in 0.083176 seconds

Naive: 3649023680.704793 (1021600484.370466) in 0.041219 seconds

SVM: 5817131318.486010 (1454335763.390944) in 0.044825 seconds

Ada: 1022540011.988822 (407906261.283972) in 0.302022 seconds

Tree: 1709270763.177791 (294314053.687804) in 0.017814 seconds

Forest: 865948793.183670 (397233796.258241) in 1.088624 seconds

GBoost: 778348874.875873 (314733456.217197) in 0.492180 seconds

XGBoost: 1055015638.687999 (377350793.401314) in 0.586652 seconds

LGBoost: 877619178.062008 (311547130.916242) in 0.271566 seconds

plot_model_scores(scores)

Pipeline

We are now ready to pick a model.

# Set model

model = LGBMRegressor()

We need to choose a cross-validation procedure to test our model.

cv = KFold()

Finally, we can combine all the parts into a single pipeline.

final_pipeline = Pipeline(steps=[

('preprocess', preprocess),

('model', model)

])

Now we can decide which parts of the pipeline to test.

# Select parameters to explore

param_grid = {'preprocess__num__ii': [SimpleImputer(), KNNImputer(), IterativeImputer()],

'preprocess__cat__si__strategy': ["most_frequent", "constant"],

'model__learning_rate': [0.1, 0.2],

'model__subsample': [1.0, 0.5],

'model__max_depth': [30, -1]}

We now generate a grid of parameters we want to search over.

# Save pipeline

grid_search = GridSearchCV(final_pipeline,

param_grid,

cv=cv,

n_jobs=-1,

scoring='neg_mean_squared_error',

verbose=3)

We fit the pipeline and pick the best estimator, from the cross-validation score.

# Fit pipeline

grid_search.fit(X_train, y_train)

grid_search.best_estimator_

Fitting 5 folds for each of 48 candidates, totalling 240 fits

Pipeline(steps=[('preprocess',

ColumnTransformer(transformers=[('num',

Pipeline(steps=[('ii',

SimpleImputer()),

('ss',

StandardScaler())]),

['MSSubClass', 'LotFrontage',

'LotArea', 'OverallQual',

'OverallCond', 'YearBuilt',

'YearRemodAdd', 'MasVnrArea',

'BsmtFinSF1', 'BsmtFinSF2',

'BsmtUnfSF', 'TotalBsmtSF',

'1stFlrSF', '2ndFlrSF',

'LowQualFinSF', 'GrLivArea',

'BsmtFull...

'LotConfig', 'LandSlope',

'Neighborhood', 'Condition1',

'Condition2', 'BldgType',

'HouseStyle', 'RoofStyle',

'RoofMatl', 'Exterior1st',

'Exterior2nd', 'MasVnrType',

'ExterQual', 'ExterCond',

'Foundation', 'BsmtQual',

'BsmtCond', 'BsmtExposure',

'BsmtFinType1',

'BsmtFinType2', 'Heating',

'HeatingQC', 'CentralAir',

'Electrical', ...])])),

('model', LGBMRegressor(max_depth=30))])

We have three ways of testing the quality of fit of our model:

- score on the training data

- score on the validation data

- score on the test data

Score on the training data: this is a biased score since we have picked the model that was best fitting the training data. Kfold cross-validation is efficient in terms of data use, but still evaluates the model over the same data it was trained.

# Cross/validation score

y_train_hat = grid_search.best_estimator_.predict(X_train)

train_rmse = mean_squared_error(y_train, y_train_hat, squared=False)

print('RMSE on training data :', train_rmse)

RMSE on training data : 12343.48585393485

Score on the validation data: this is an unbiased score since we have left out this sample exactly for this purpose. However, be aware that the validation score is unbiased on on the first run. Once we change the grid and pick the algorithm based on previous validation data scores, also this score becomes biased.

# Validation set score

y_validation_hat = grid_search.best_estimator_.predict(X_validation)

validation_rmse = mean_squared_error(y_validation, y_validation_hat, squared=False)

print('RMSE on validation data :', validation_rmse)

RMSE on validation data : 26213.18659495431

Final predictions: we can now use our model to output the predictions.

# Validation score

y_test_hat = grid_search.best_estimator_.predict(X_test)